Estimating tail risk

Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

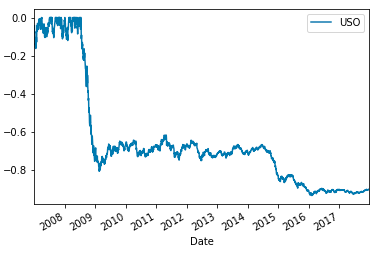

Historical drawdown

Historical Drawdown of the USO Oil ETF

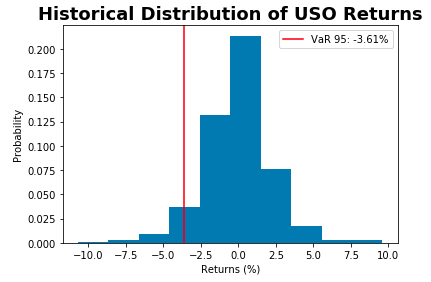

Historical Value at Risk

95% certain that losses will not exceed -2.3% in a given day based on historical values.

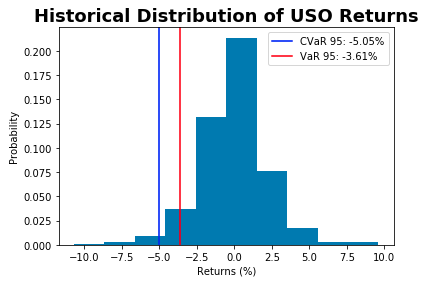

Historical expected shortfall

In the worst 5% of cases, losses were on average exceed -2.5% historically.