Correlation and co-variance

Introduction to Portfolio Risk Management in Python

Dakota Wixom

Quantitative Analyst | QuantCourse.com

Pearson correlation

Examples of different correlations between two random variables:

Pearson correlation

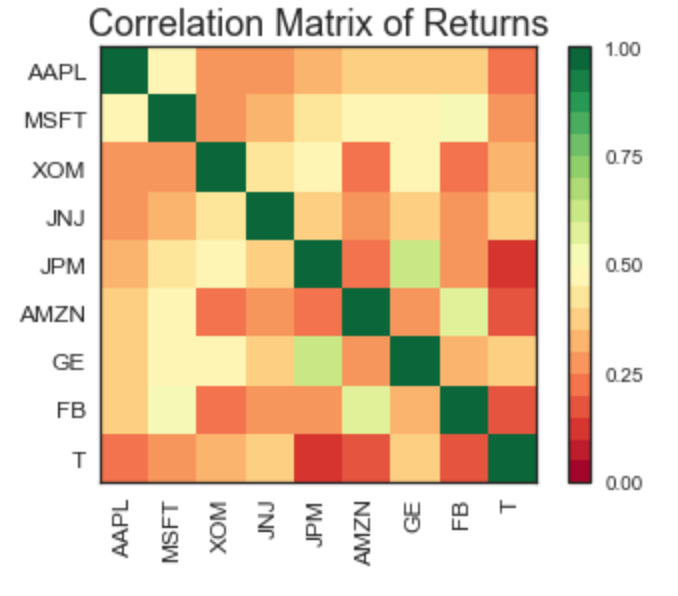

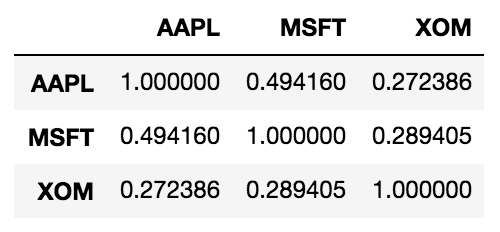

A heatmap of a correlation matrix:

Correlation matrix in Python

Assuming StockReturns is a pandas DataFrame of stock returns, you can calculate the correlation matrix as follows:

correlation_matrix = StockReturns.corr()

print(correlation_matrix)

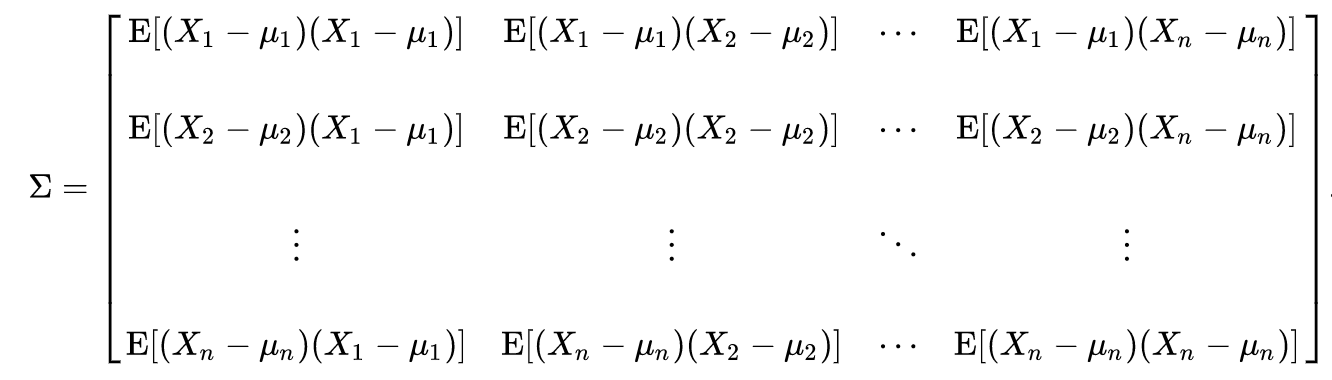

The Co-variance matrix

To calculate the co-variance matrix ($ \Sigma $) of returns X:

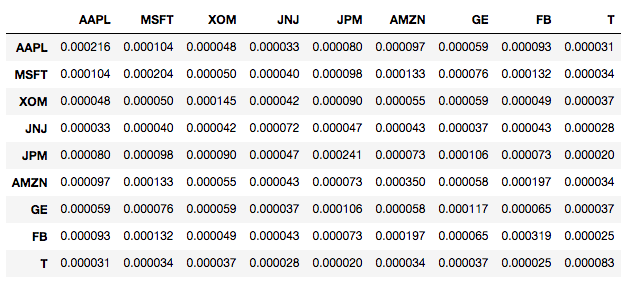

The Co-variance matrix in Python

Assuming StockReturns is a pandas DataFrame of stock returns, you can calculate the covariance matrix as follows:

cov_mat = StockReturns.cov()

cov_mat

Matrix transpose

Examples of matrix transpose operations:

![]()

Dot product

The dot product operation of two vectors a and b: