อัตราการอนุมัติสินเชื่อ

การสร้างโมเดลความเสี่ยงด้านเครดิตด้วย Python

Michael Crabtree

Data Scientist, Ford Motor Company

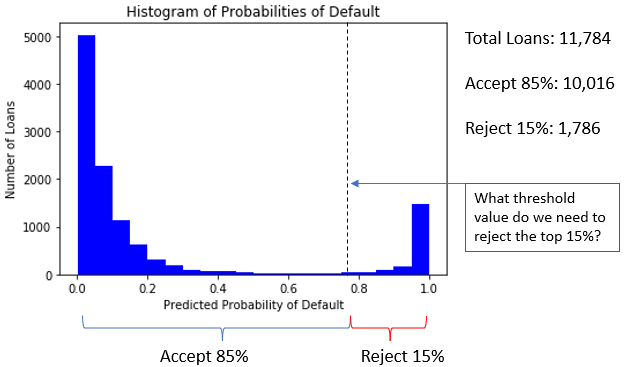

ทำความเข้าใจอัตราการอนุมัติ

- ตัวอย่าง: อนุมัติ 85% ของสินเชื่อที่มีค่า

prob_defaultต่ำที่สุด

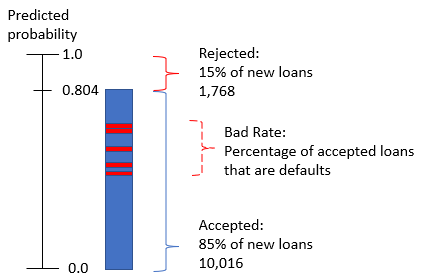

Bad Rate

- แม้จะใช้ threshold ที่คำนวณแล้ว สินเชื่อที่อนุมัติบางส่วนก็ยังเป็นการผิดนัด

- สินเชื่อเหล่านี้มีค่า

prob_defaultอยู่ในช่วงที่โมเดลยังปรับเทียบได้ไม่ดี

การคำนวณ bad rate

#Calculate the bad rate

np.sum(accepted_loans['true_loan_status']) / accepted_loans['true_loan_status'].count()

- ถ้า non-default คือ

0และ default คือ1แล้วsum()จะเป็นจำนวนนับของการผิดนัด .count()ของคอลัมน์เดียวเท่ากับจำนวนแถวทั้งหมดของ data frame