Cleaning and improving your data

Machine Learning for Time Series Data in Python

Chris Holdgraf

Fellow, Berkeley Institute for Data Science

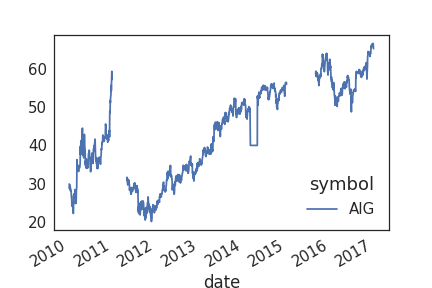

What messy data looks like

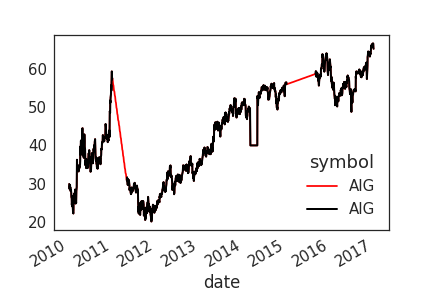

Visualizing the interpolated data

Applying this to our data

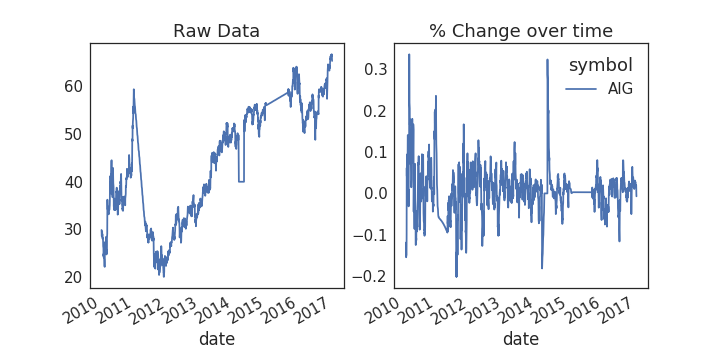

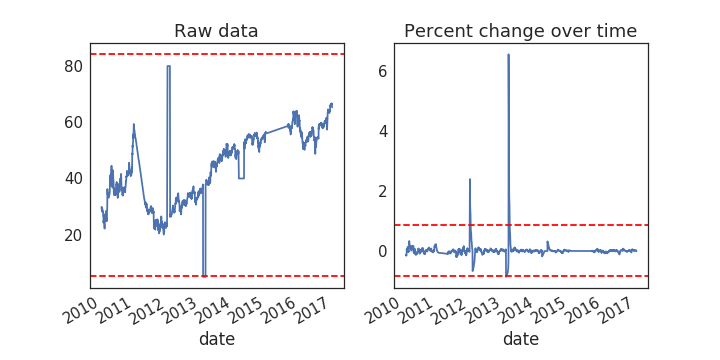

# Plot the raw data

fig, axs = plt.subplots(1, 2, figsize=(10, 5))

ax = prices.plot(ax=axs[0])

# Calculate % change and plot

ax = prices.rolling(window=20).aggregate(percent_change).plot(ax=axs[1])

ax.legend_.set_visible(False)

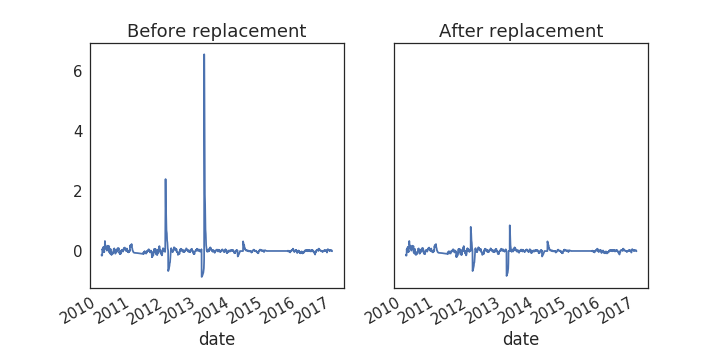

Visualizing outlier thresholds

Visualize the results

fig, axs = plt.subplots(1, 2, figsize=(10, 5))

prices_outlier_centered.plot(ax=axs[0])

prices_outlier_fixed.plot(ax=axs[1])