Machine learning for MPT

Machine Learning for Finance in Python

Nathan George

Data Science Professor

Plot the results

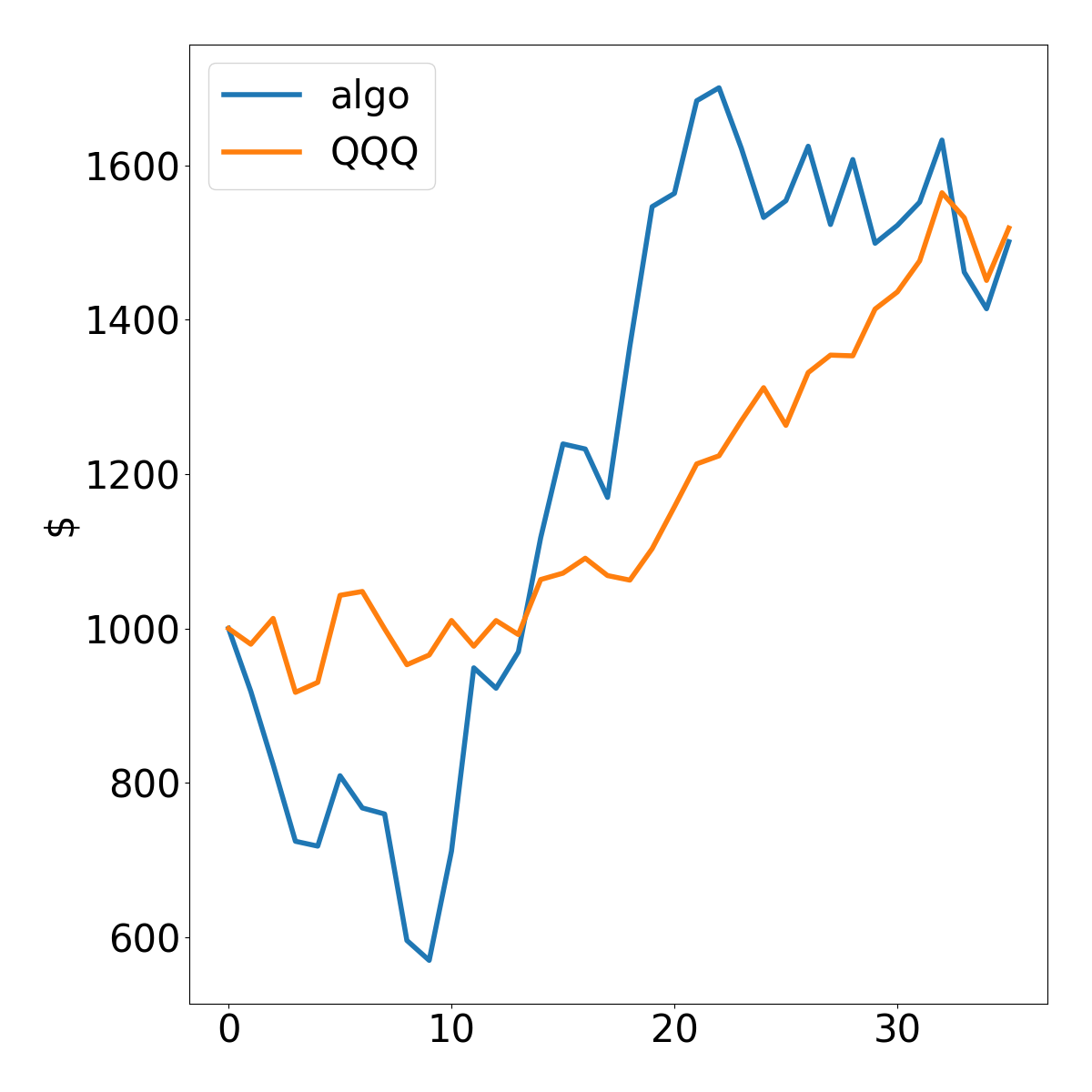

plt.plot(algo_cash, label='algo')

plt.plot(qqq_cash, label='QQQ')

plt.ylabel('$')

plt.legend() # show the legend

plt.show()

Machine Learning for Finance in Python

Nathan George

Data Science Professor

plt.plot(algo_cash, label='algo')

plt.plot(qqq_cash, label='QQQ')

plt.ylabel('$')

plt.legend() # show the legend

plt.show()