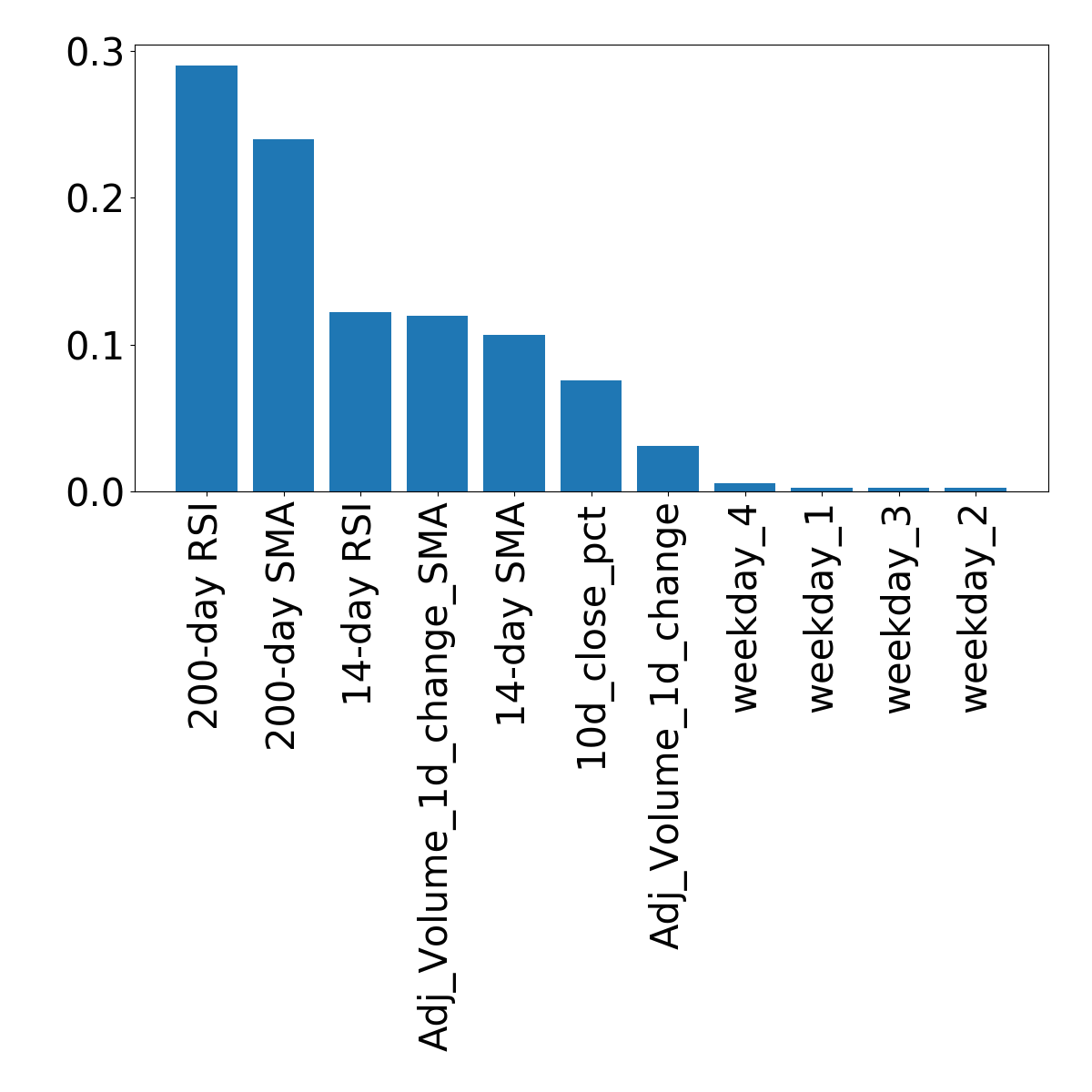

# feature importances from random forest model

importances = random_forest.feature_importances_

# index of greatest to least feature importances

sorted_index = np.argsort(importances)[::-1]

x = range(len(importances))

# create tick labels

labels = np.array(feature_names)[sorted_index]

plt.bar(x, importances[sorted_index], tick_label=labels)

# rotate tick labels to vertical

plt.xticks(rotation=90)

plt.show()