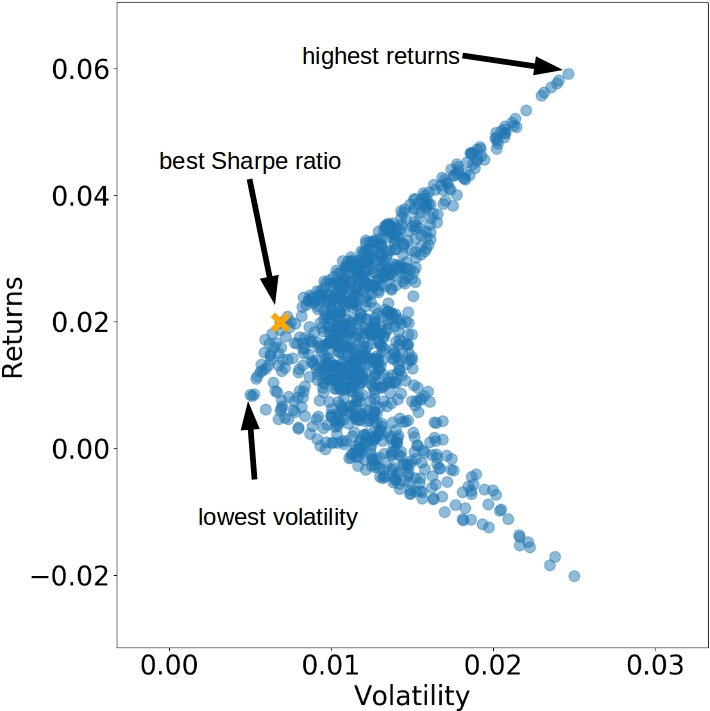

# empty dictionaries for sharpe ratios and best sharpe indexes by date

sharpe_ratio, max_sharpe_idxs = {}, {}

# loop through dates and get sharpe ratio for each portfolio

for date in portfolio_returns.keys():

for i, ret in enumerate(portfolio_returns[date]):

volatility = portfolio_volatility[date][i]

sharpe_ratio.setdefault(date,[]).append(ret / volatility)

# get the index of the best sharpe ratio for each date

max_sharpe_idxs[date] = np.argmax(sharpe_ratio[date])

Create features

# calculate exponentially-weighted moving average of daily returns

ewma_daily = returns_daily.ewm(span=30).mean()

# resample daily returns to first business day of the month

ewma_monthly = ewma_daily.resample('BMS').first()

# shift ewma 1 month forward

ewma_monthly = ewma_monthly.shift(1).dropna()

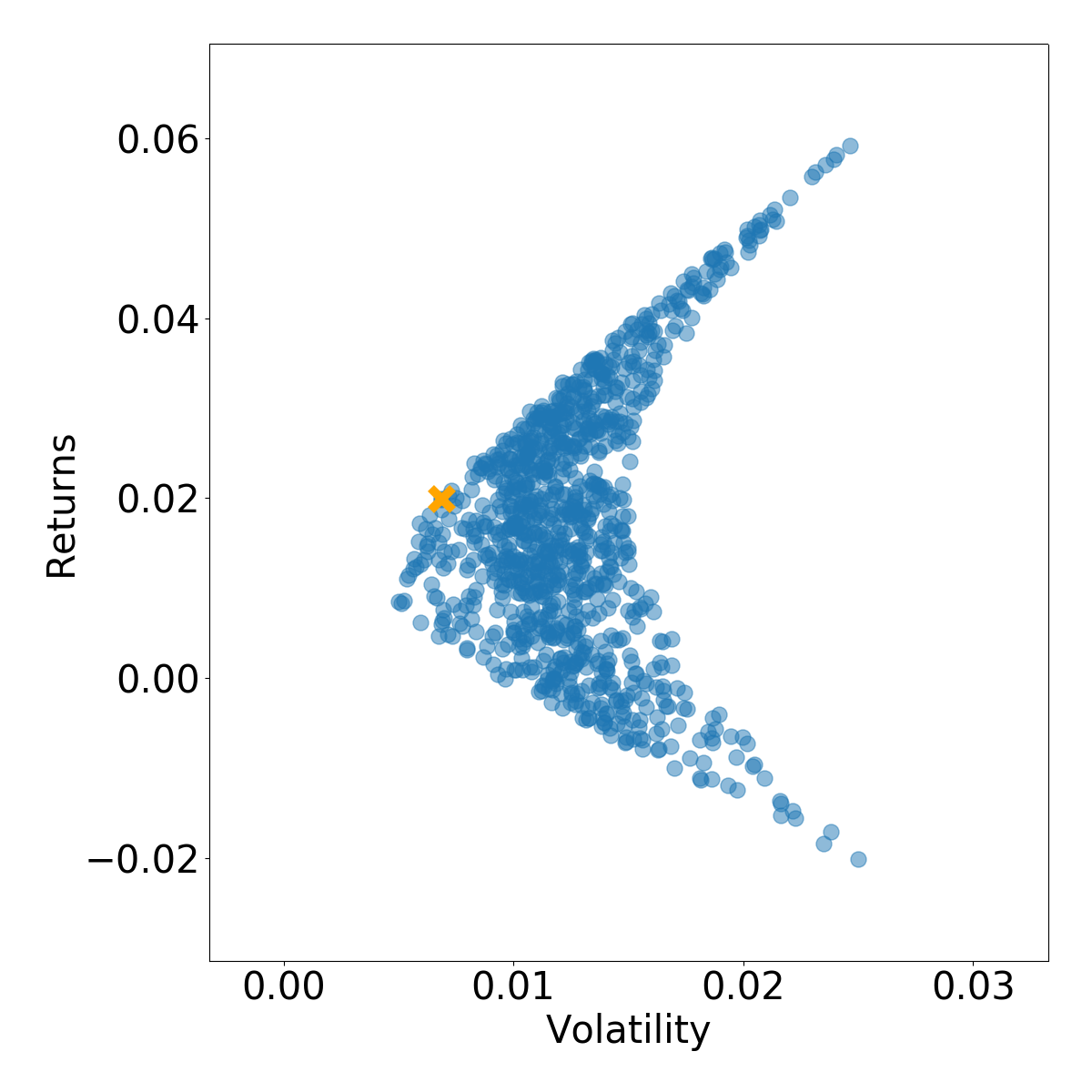

Calculate features and targets

targets, features = [], []

# create features from price history and targets as ideal portfolio

for date, ewma in ewma_monthly.iterrows():

# get the index of the best sharpe ratio

best_idx = max_sharpe_idxs[date]

targets.append(portfolio_weights[date][best_idx])

features.append(ewma)

targets = np.array(targets)

features = np.array(features)