Custom loss functions

Machine Learning for Finance in Python

Nathan George

Data Science Professor

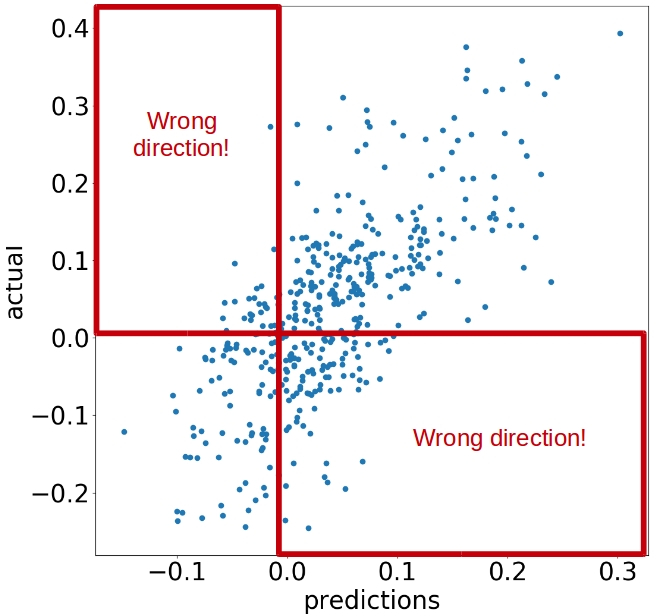

The bow-tie shape

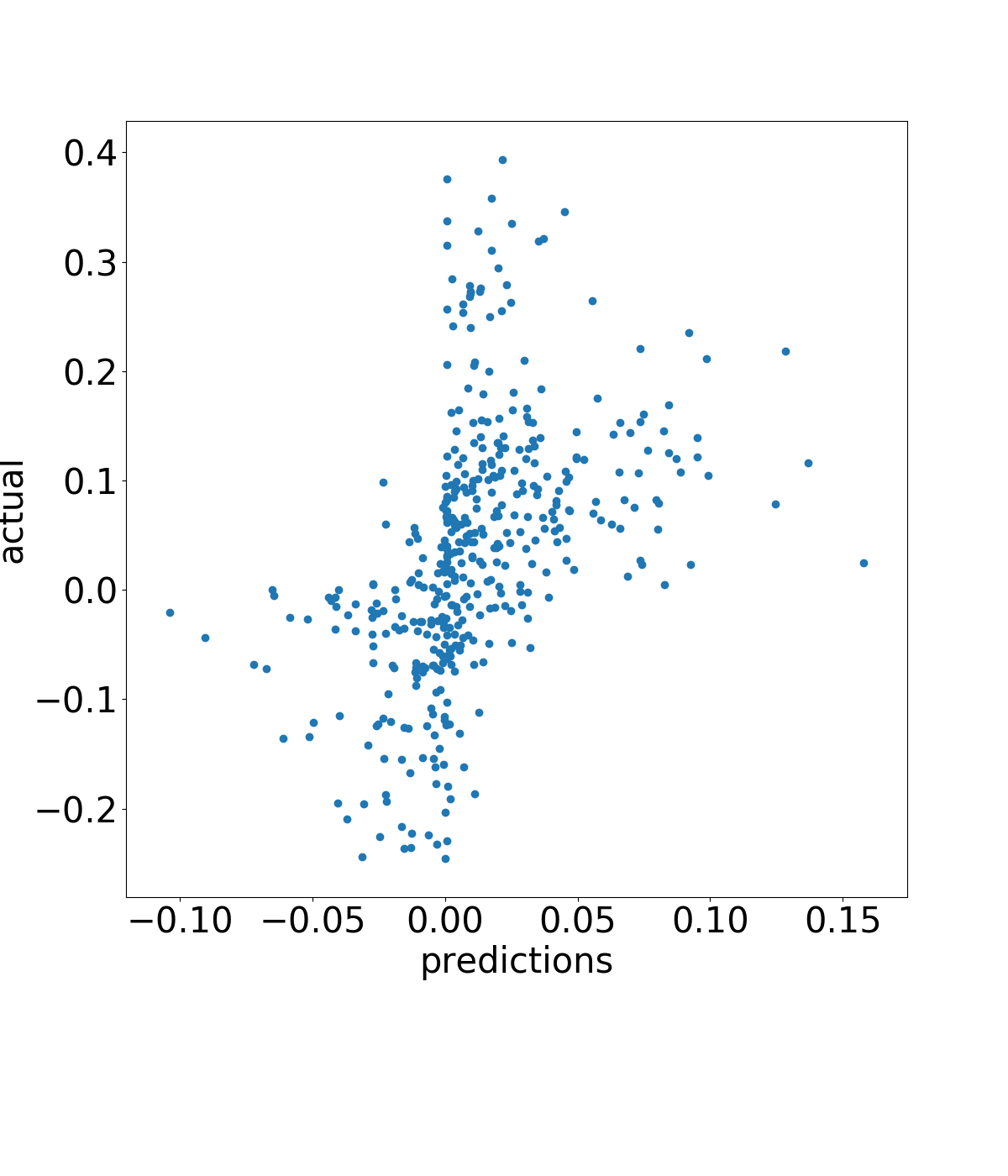

train_preds = model.predict(scaled_train_features)

# scatter the predictions vs actual

plt.scatter(train_preds, train_targets)

plt.xlabel('predictions')

plt.ylabel('actual')

plt.show()