Machine Learning for Finance in Python

Nathan George

Data Science Professor

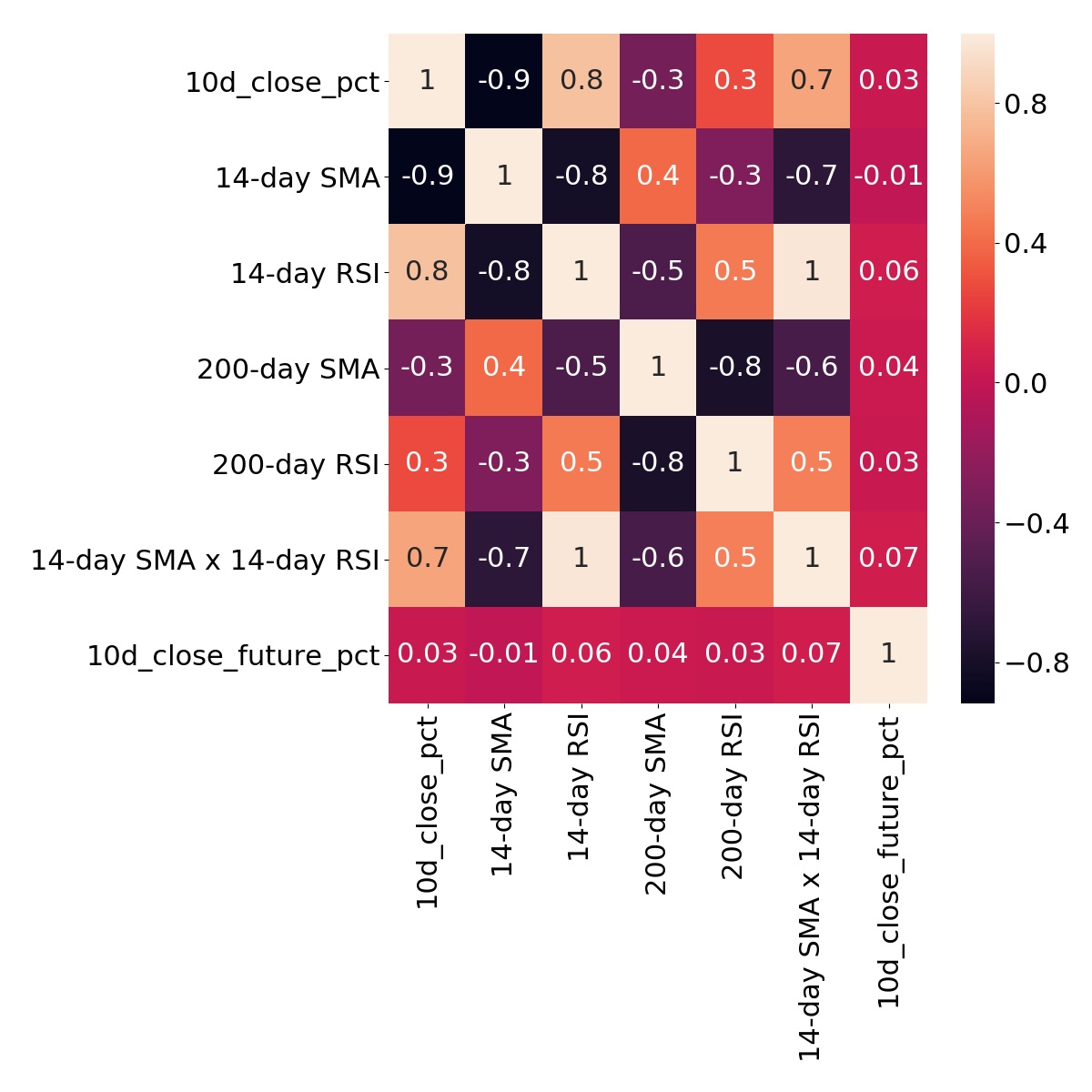

# add non-linear interaction term for a linear model SMAxRSI = amd_df['14-day SMA'] * amd_df['14-day RSI']

Some models that don't require manually creating interaction features:

Decision-tree-based models

Others

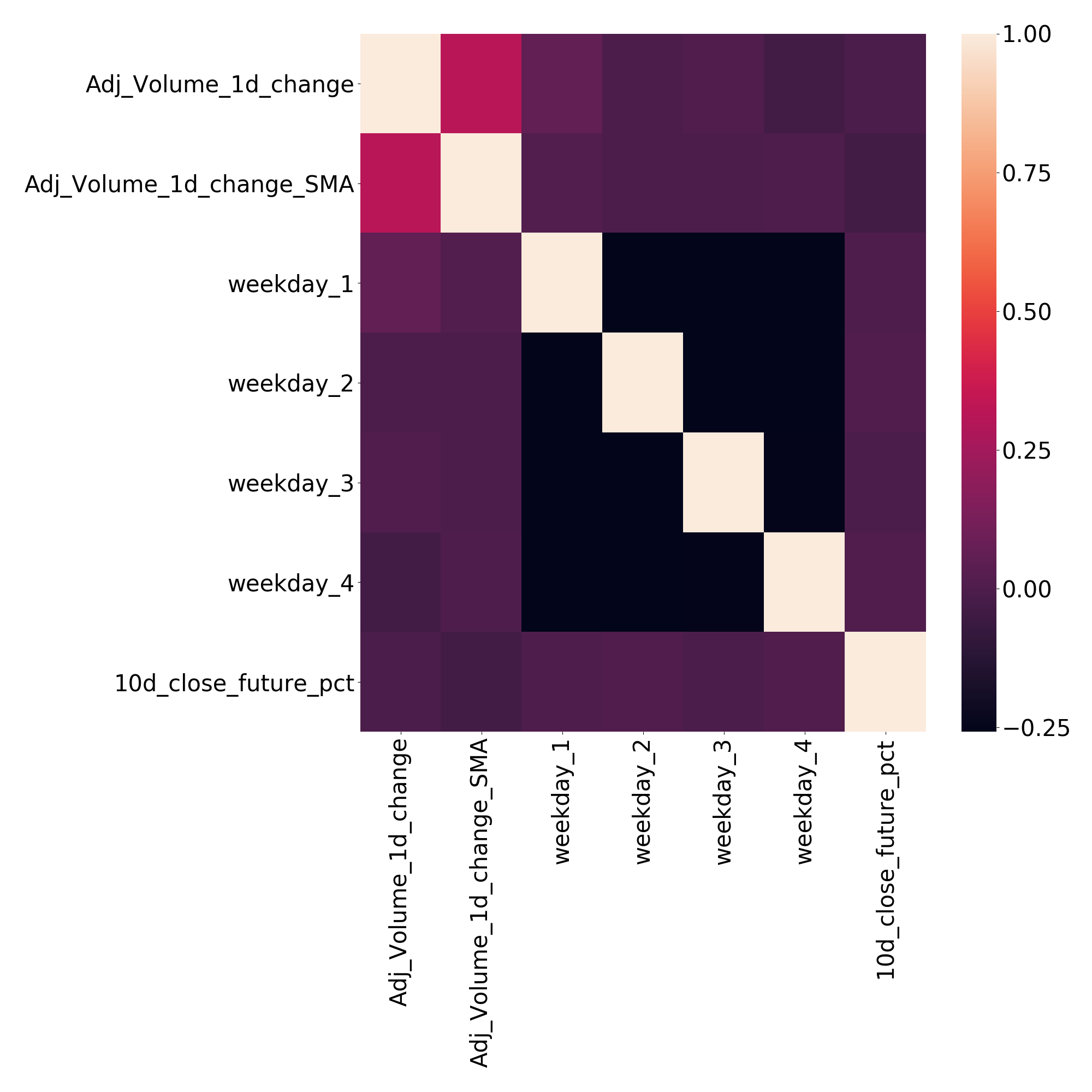

amd_df['Adj_Volume_1d_change'] = amd_df['Adj_Volume'].pct_change() one_day_change = amd_df['Adj_Volume_1d_change'].values amd_df['Adj_Volume_1d_change_SMA'] = talib.SMA(one_day_change, timeperiod=10)

amd_df['Adj_Volume_1d_change'] = amd_df['Adj_Volume'].pct_change()

one_day_change = amd_df['Adj_Volume_1d_change'].values amd_df['Adj_Volume_1d_change_SMA'] = talib.SMA(one_day_change, timeperiod=10)

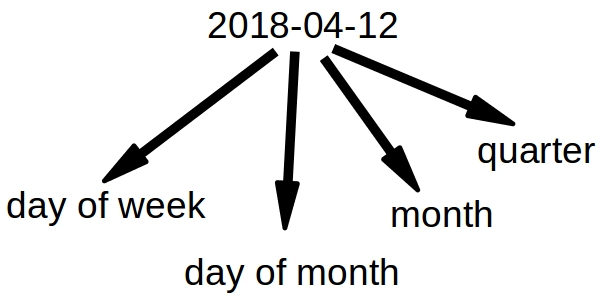

print(amd_df.index.dayofweek)

Int64Index([2, 3, 4, 0, 1, 2, 3, 4, 0, 1, ... 1, 2, 3, 4, 0, 1, 2, 3, 4, 0], dtype='int64', name='Date', length=4807)

days_of_week = pd.get_dummies(amd_df.index.dayofweek, prefix='weekday', drop_first=True) print(days_of_week.head())

days_of_week = pd.get_dummies(amd_df.index.dayofweek, prefix='weekday', drop_first=True)

print(days_of_week.head())

weekday_1 weekday_2 weekday_3 weekday_4 Date 2018-04-10 1 0 0 0 2018-04-11 0 1 0 0 2018-04-12 0 0 1 0 2018-04-13 0 0 0 1 2018-04-16 0 0 0 0