Machine Learning for Finance in Python

Nathan George

Data Science Professor

print(feature_names)

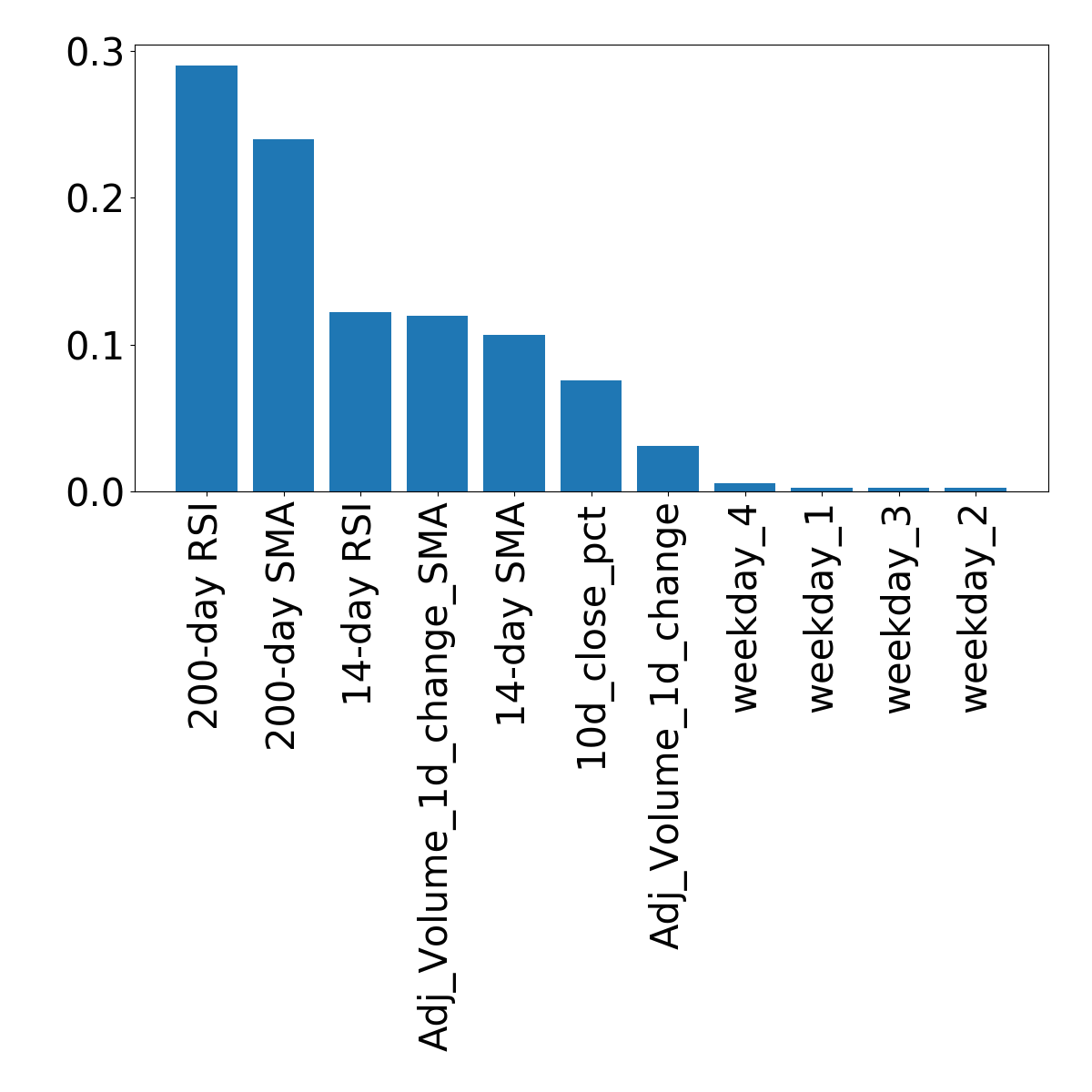

['10d_close_pct', '14-day SMA', '14-day RSI', '200-day SMA', '200-day RSI', 'Adj_Volume_1d_change', 'Adj_Volume_1d_change_SMA', 'weekday_1', 'weekday_2', 'weekday_3', 'weekday_4']

print(feature_names[:-4])

['10d_close_pct', '14-day SMA', '14-day RSI', '200-day SMA', '200-day RSI', 'Adj_Volume_1d_change', 'Adj_Volume_1d_change_SMA']

train_features = train_features.iloc[:, :-4] test_features = test_features.iloc[:, :-4]

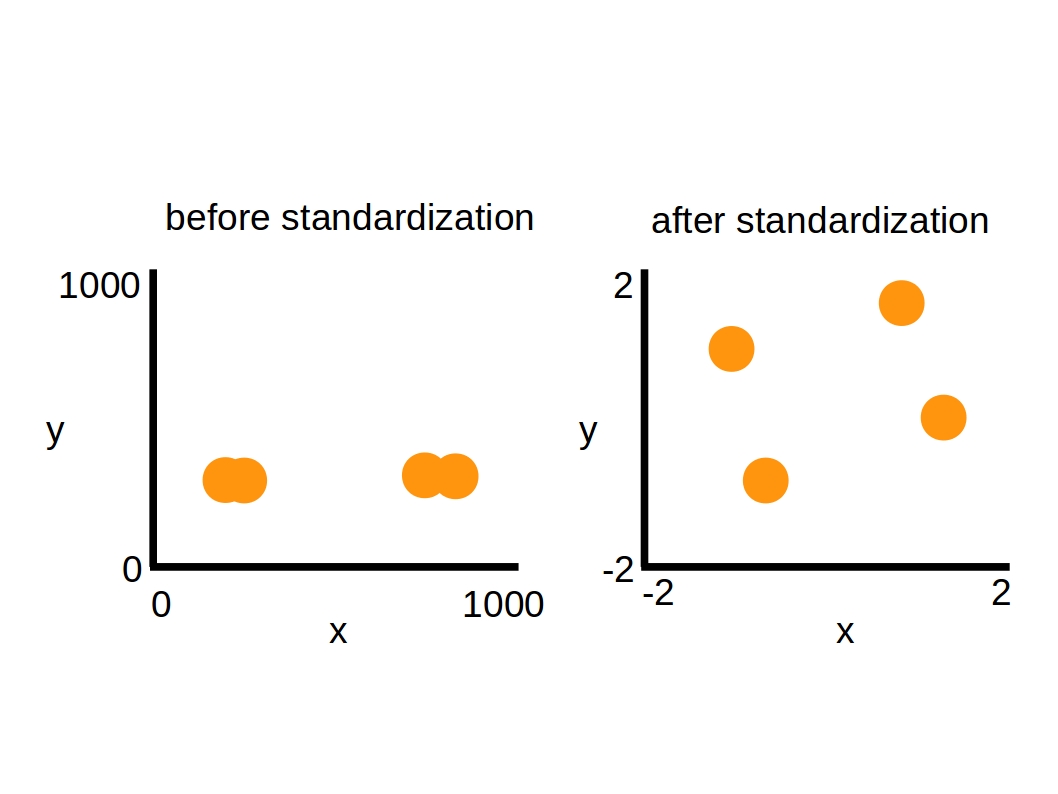

Scaling options:

from sklearn.preprocessing import scale sc = scale() scaled_train_features = sc.fit_transform(train_features) scaled_test_features = sc.transform(test_features)

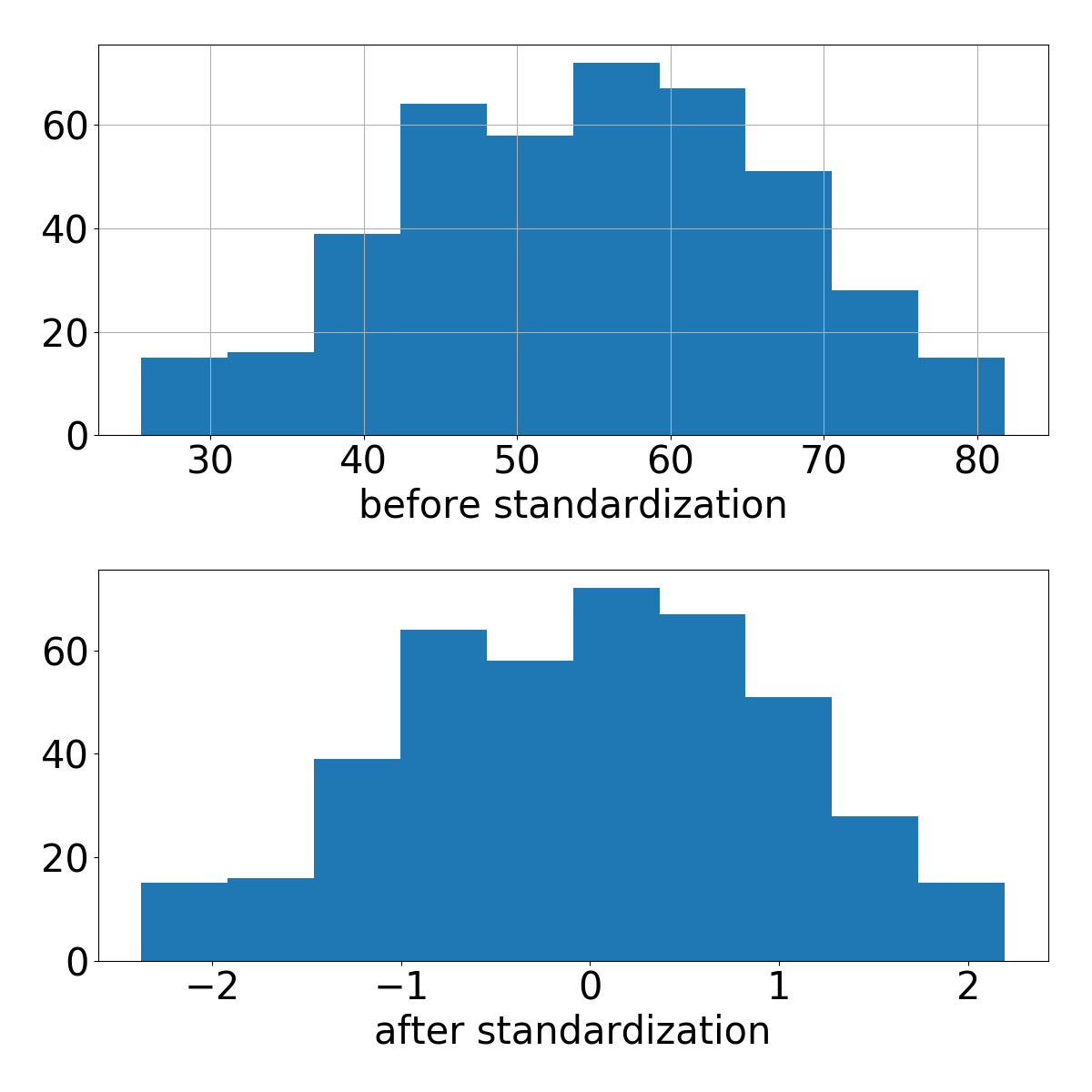

# create figure and list containing axes f, ax = plt.subplots(nrows=2, ncols=1) # plot histograms of before and after scaling train_features.iloc[:, 2].hist(ax=ax[0]) ax[1].hist(scaled_train_features[:, 2]) plt.show()

# create figure and list containing axes f, ax = plt.subplots(nrows=2, ncols=1)

# plot histograms of before and after scaling train_features.iloc[:, 2].hist(ax=ax[0]) ax[1].hist(scaled_train_features[:, 2]) plt.show()