Model extensions part 2: Lagged effects

Building Response Models in R

Kathrin Gruber

Assistant Professor of Econometrics Erasmus University Rotterdam

What's the value added?

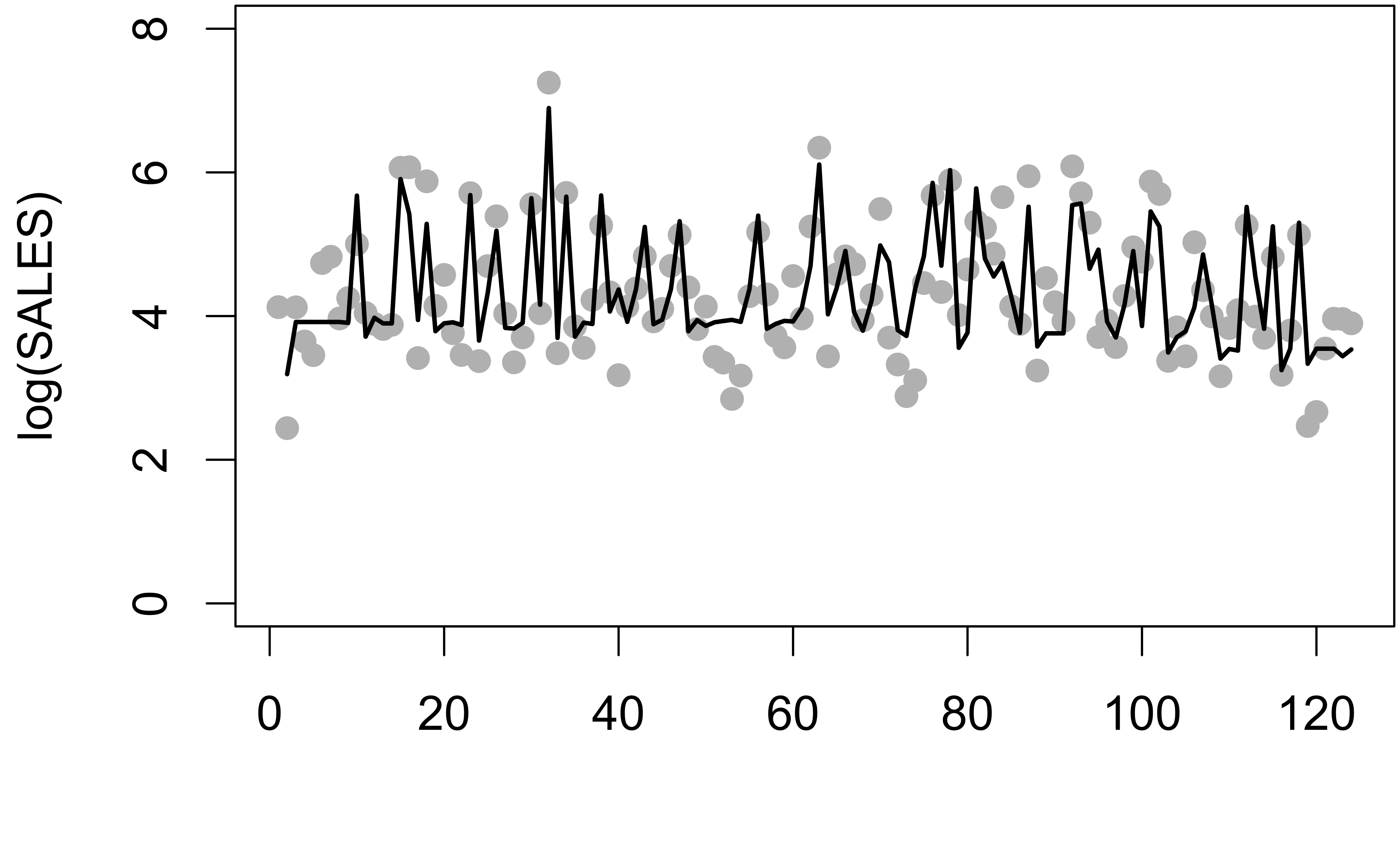

lag.model <- lm(log(SALES) ~ PRICE + Price.lag + DISPLAY + Display.lag + COUPON + Coupon.lag + DISPLAYCOUPON + DisplayCoupon.lag, data = sales.data)plot(log(SALES) ~ 1, data = sales.data) lines(c(NA, fitted.values(lag.model)) ~ 1)