Model risk is the risk of using the wrong model

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

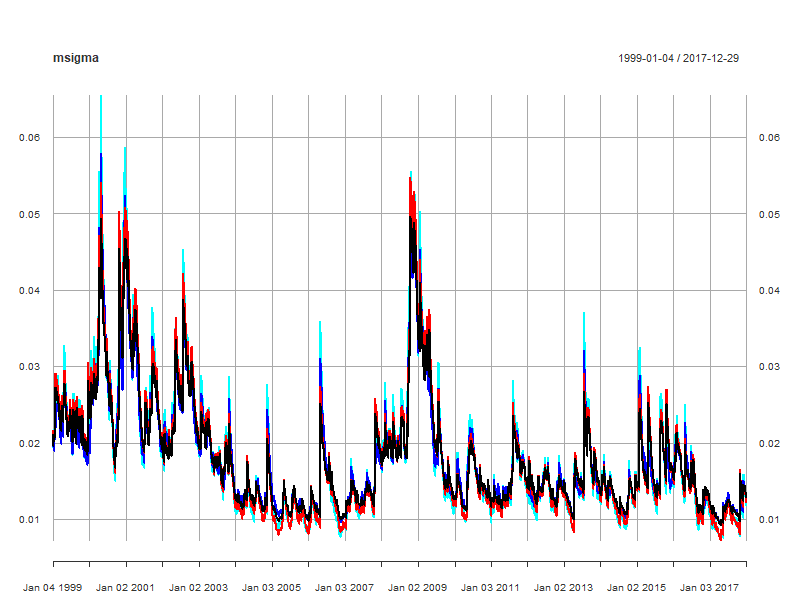

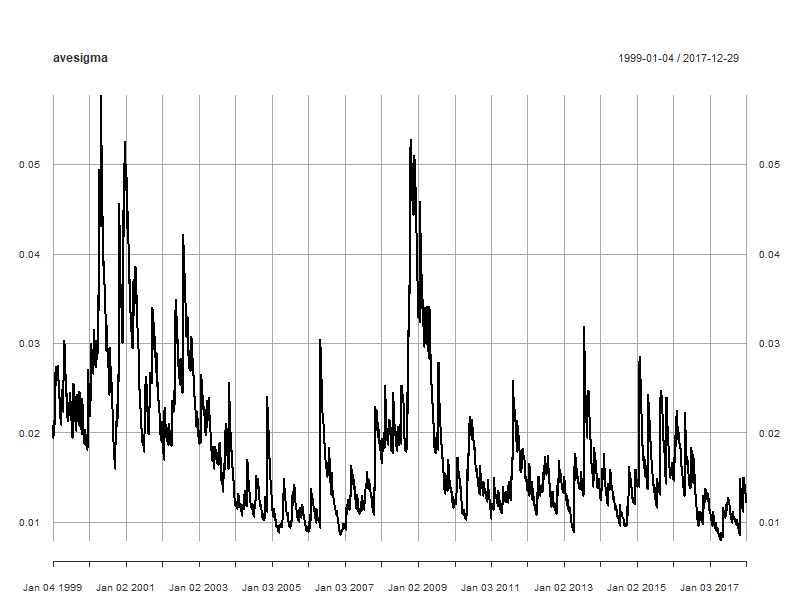

The average vol prediction

avesigma <- xts(rowMeans(msigma), order.by = time(msigma))

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

avesigma <- xts(rowMeans(msigma), order.by = time(msigma))