Value-at-risk

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

Value-at-risk

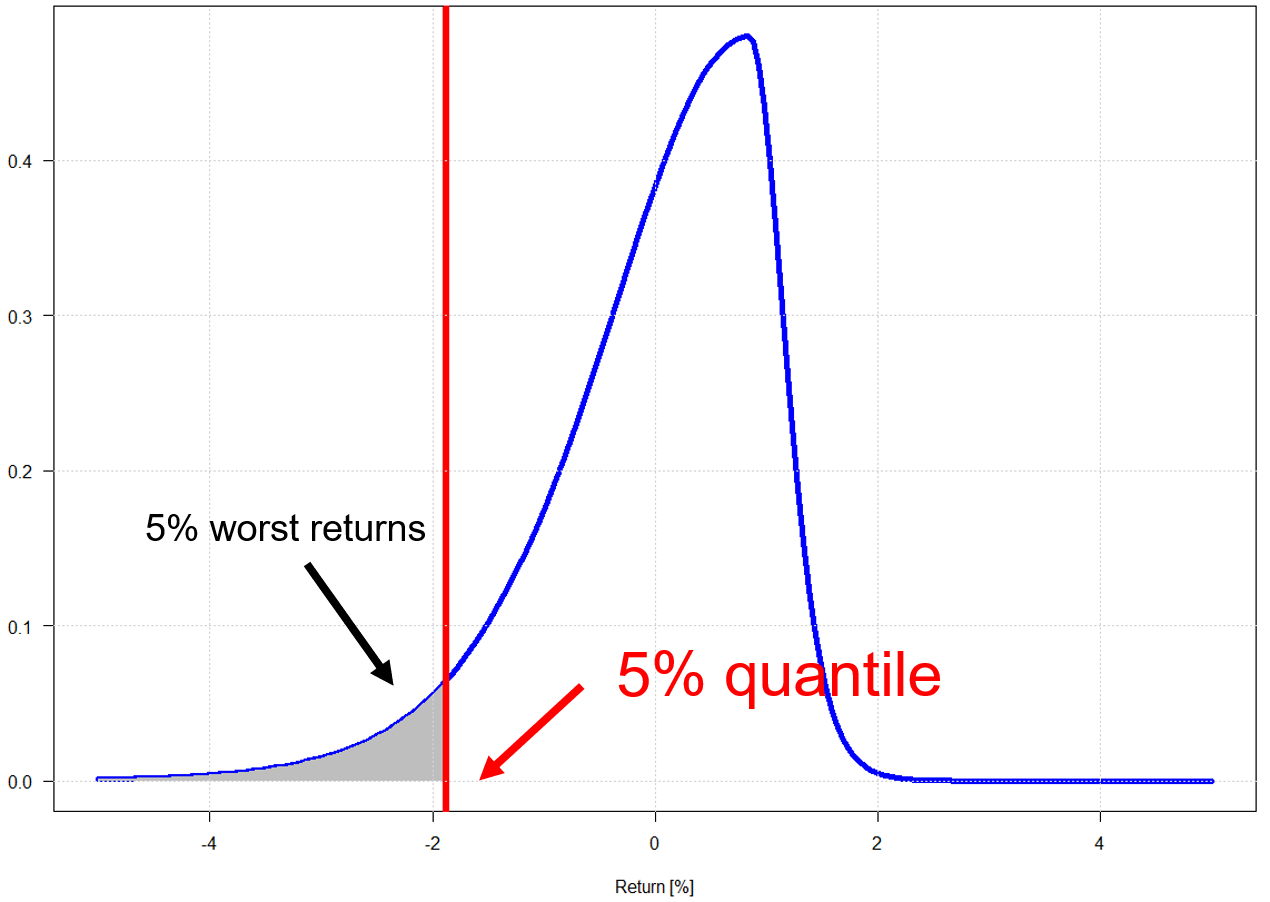

- A popular measure of downside risk: 5% value-at-risk. The 5% quantile of the return distribution represents the best return in the 5% worst scenarios.

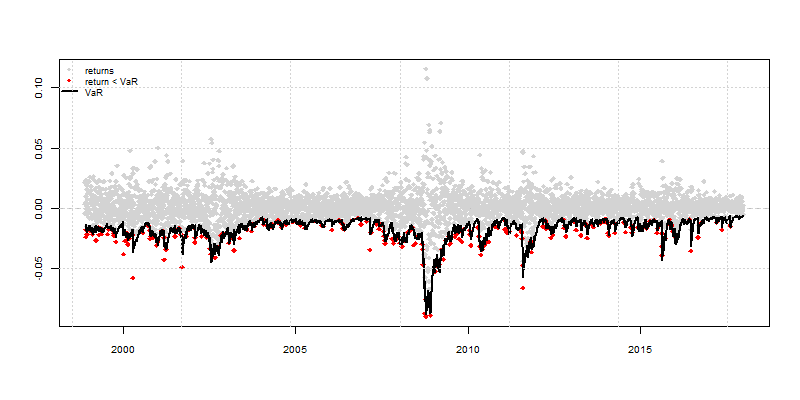

Value-at-risk plot for loss probability 5%

actual <- xts(as.data.frame(garchroll)$Realized, time(garchVaR))

VaRplot(alpha = 0.05, actual = actual, VaR = garchVaR)