GARCH models: The way forward

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

Inventors of GARCH models

Robert Engle

Tim Bollerslev

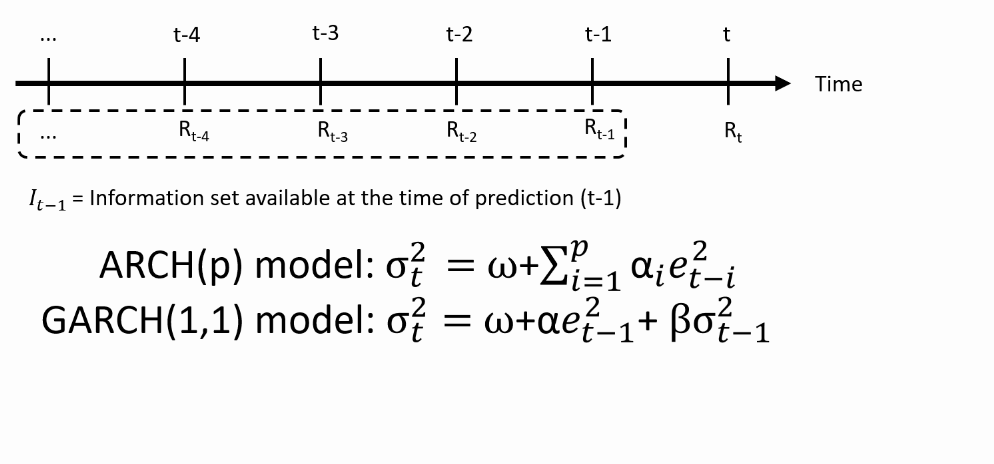

Notation (i)

- Input: Time series of returns

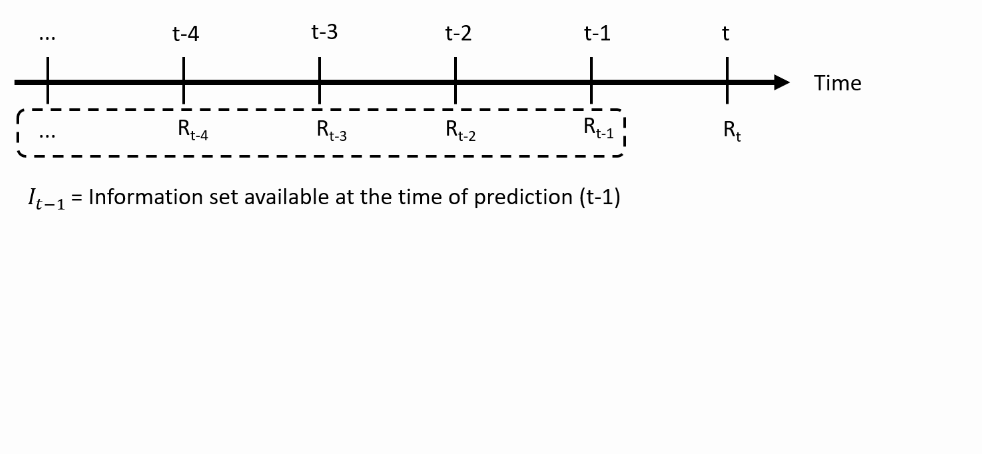

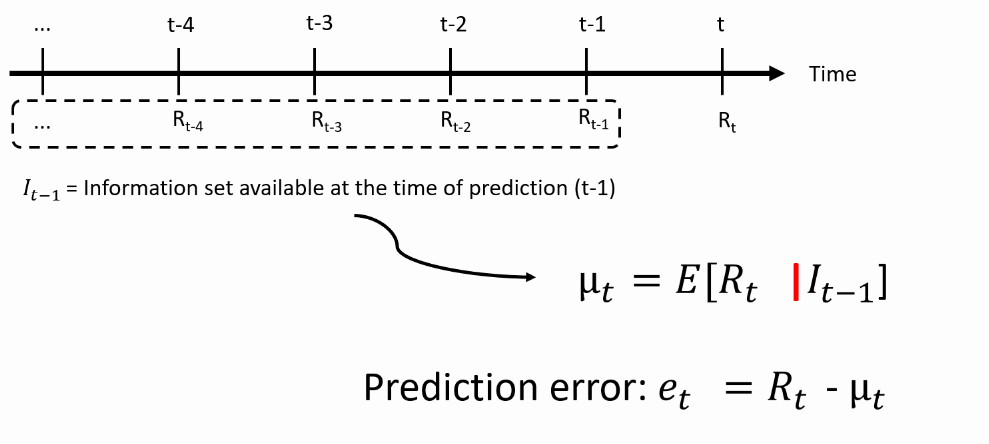

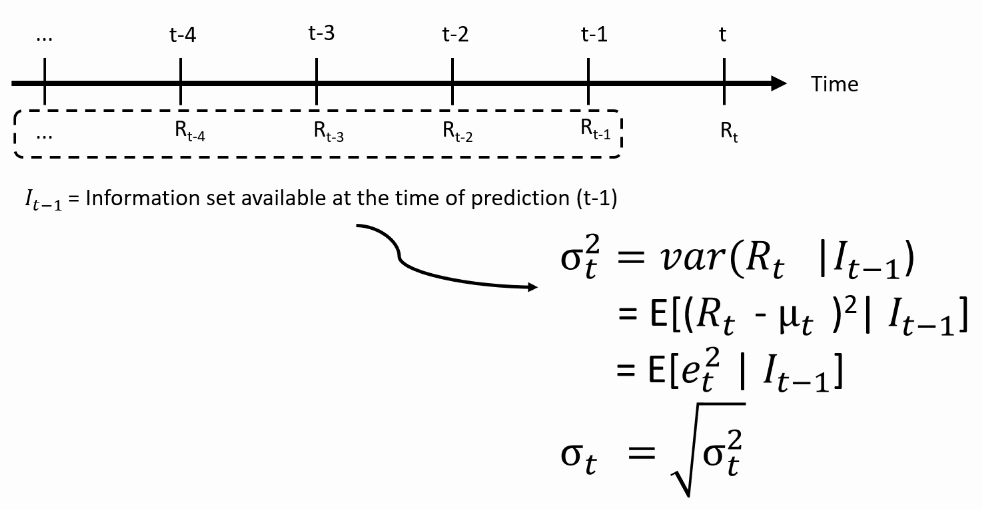

Notation (ii)

- At time $t-1$, you make the prediction about the the future return $R_t$, using the information set available at time $t-1$:

Notation (iii)

- Predicting the mean return: what is the best possible prediction of the actual return?

Notation (iv)

- We then predict the variance: how far off the return can be from its mean?

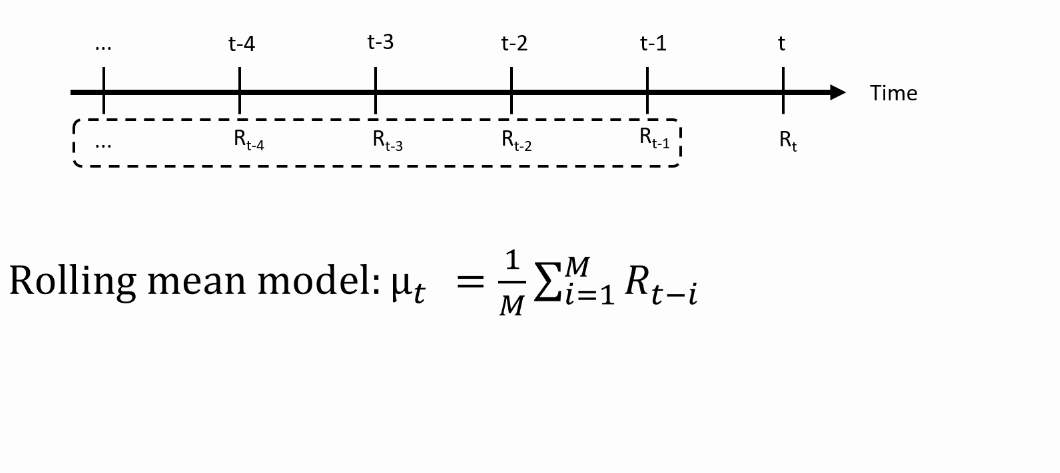

From theory to practice: Models for the mean

- We need an equation that maps the past returns into a prediction of the mean

For AR(MA) models for the mean, see Datacamp course on time series analysis.

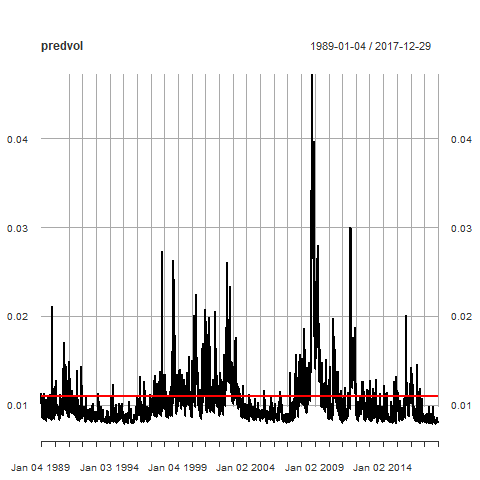

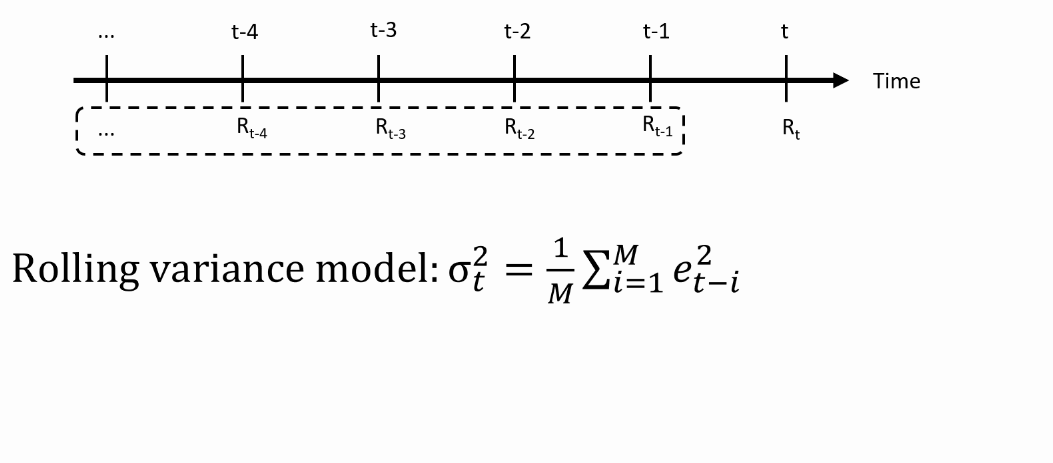

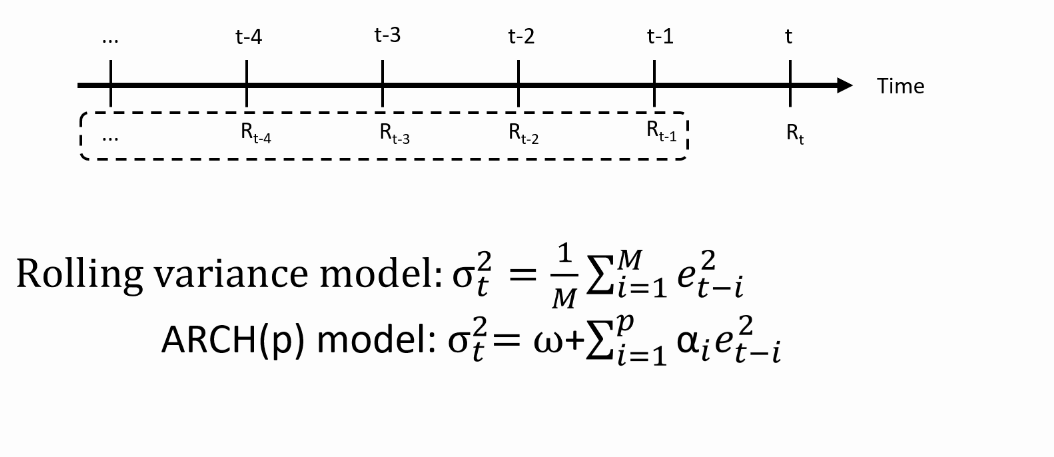

From theory to practice: Models for the variance

- We need an equation that maps the past returns into predictions of the variance

ARCH(p) model: Autoregressive Conditional Heteroscedasticity

- We need an equation that maps the past returns into predictions of the variance

GARCH(1,1) model: Generalized ARCH

- We need an equation that maps the past returns into predictions of the variance