GARCH Models in R

Kris Boudt

Professor of finance and econometrics

Change the argument distribution.model of ugarchspec() from "norm" to "sstd":

distribution.model

ugarchspec()

"norm"

"sstd"

garchspec <- ugarchspec( mean.model = list(armaOrder = c(0, 0)), variance.model = list(model = "sGARCH"), distribution.model = "norm")

$$ \downarrow$$

garchspec <- ugarchspec( mean.model = list(armaOrder = c(0, 0)), variance.model = list(model = "sGARCH"), distribution.model = "sstd")

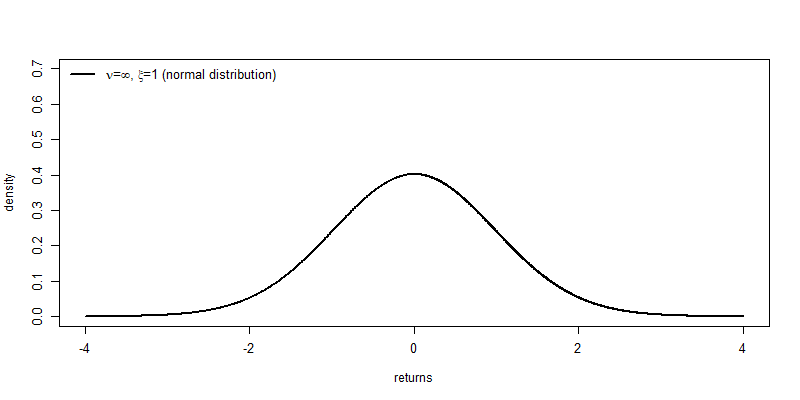

Under the model assumptions

$$ R_{t} = \mu_{t} + e_{t} $$ $$ e_{t} \sim N(0, \sigma^{2}_{t}) $$

it follows that

$$ \frac{R_{t} - \mu_{t}}{\sigma_{t}} \sim N(0, 1) $$

$$ Z_{t} = \frac{R_{t} - \hat{\mu_{t}}}{ \hat{\sigma_{t}}} $$

Calculation in R

# Obtain standardized returns stdret <- residuals(garchfit, standardize = TRUE)

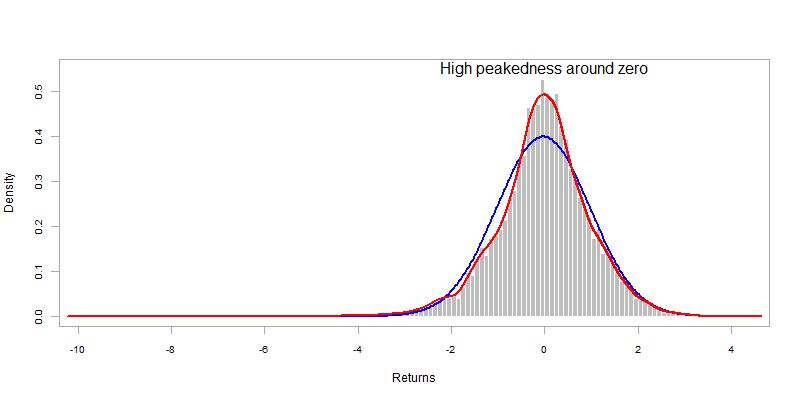

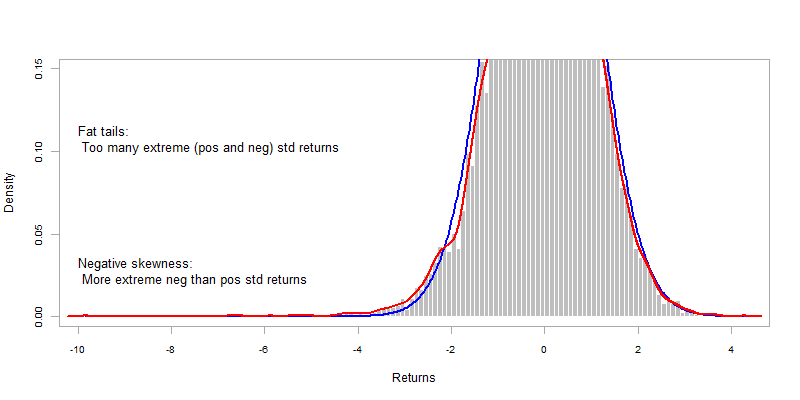

library(PerformanceAnalytics) chart.Histogram(sp500ret, methods = c("add.normal", "add.density"), colorset = c("gray", "red", "blue"))

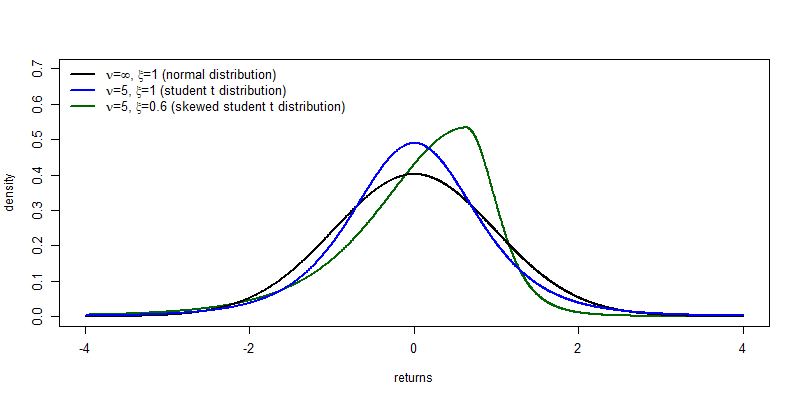

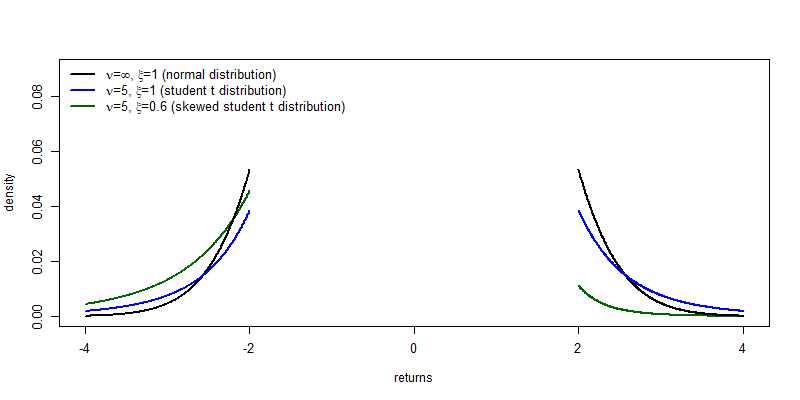

A realistic distribution thus needs to accommodate the presence of

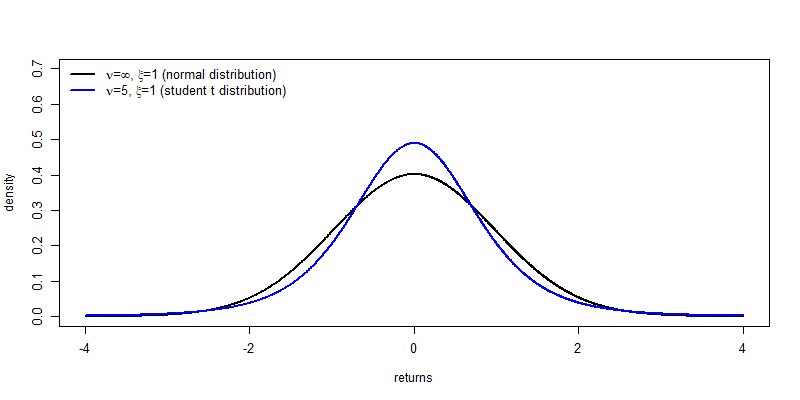

In rugarch this is possible with the skewed student t distribution:

rugarch

garchspec <- ugarchspec(distribution.model = "sstd")

Compared to the normal distribution, the skewed student t distribution has two extra parameters:

shape

skew

Special cases:

Set argument distribution.model to "sstd"

garchspec <- ugarchspec(mean.model = list(armaOrder = c(0,0)), variance.model = list(model = "sGARCH"), distribution.model = "sstd")

Estimate the model

garchfit <- ugarchfit(data = sp500ret, spec = garchspec) coef(garchfit)

mu omega alpha1 beta1 skew shape 5.669200e-04 6.281258e-07 7.462984e-02 9.223701e-01 9.436331e-01 6.318621e+00