Do the GARCH predictions fit will with the observed returns?

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

1) Goodness of fit for the mean prediction

Based on the estimated GARCH model, we have:

Implementation

e <- residuals(tgarchfit)

mean(e ^ 2)

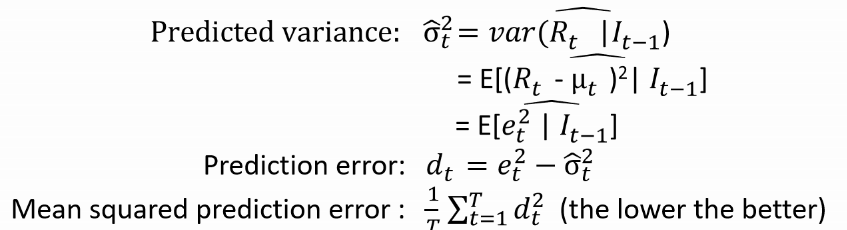

2) Goodness of fit for the variance prediction

The GARCH model leads to:

Implementation

e <- residuals(tgarchfit)

d <- e ^ 2 - sigma(tgarchfit) ^ 2

mean(d ^ 2)