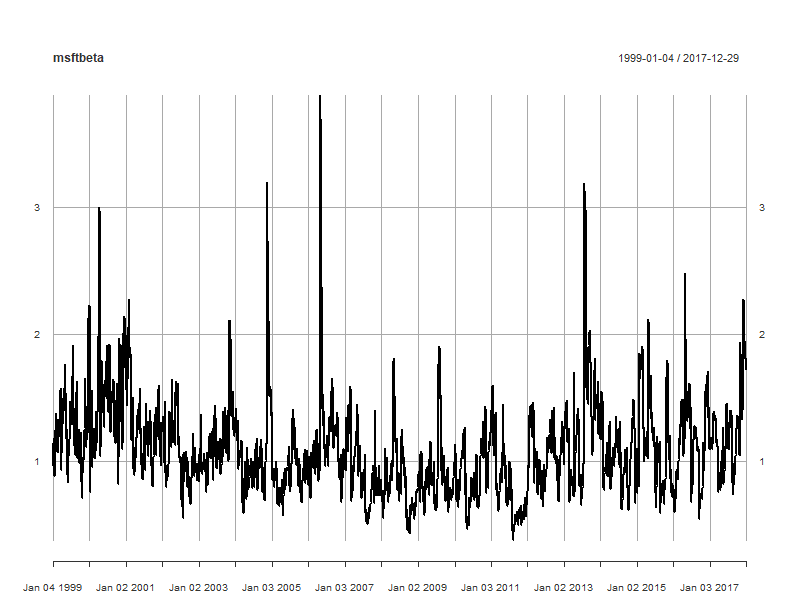

GARCH volatility leads to time-varying variability of the returns

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

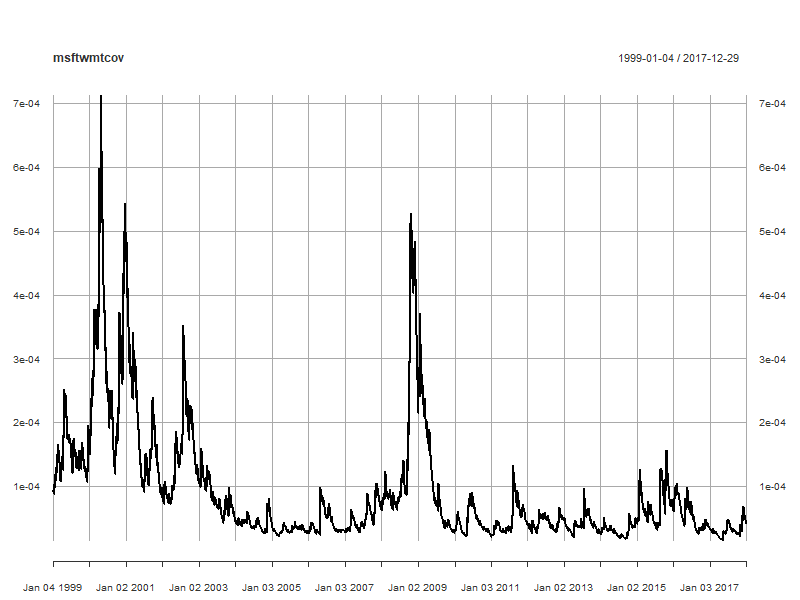

GARCH covariance estimation in four steps

Step 4: Compute the GARCH covariance by multiplying the estimated correlation and volatilities

msftwmtcov <- msftwmtcor * sigma(msftgarchfit) * sigma(wmtgarchfit)

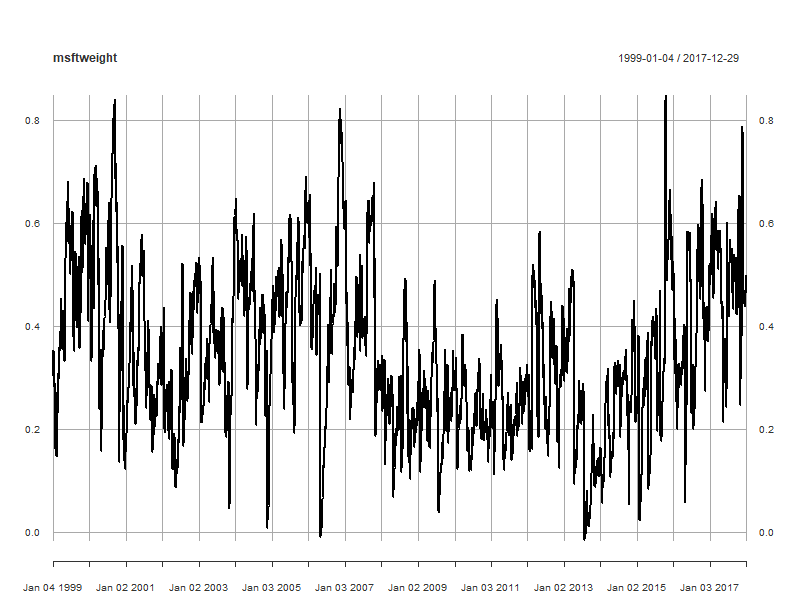

Minimum variance portfolio weights

Solution:

Calculation in R:

msftvar <- sigma(msftgarchfit) ^ 2

wmtvar <- sigma(wmtgarchfit) ^ 2

msftwmtcov <- msftwmtcor * sigma(msftgarchfit) * sigma(wmtgarchfit)

msftweight <- (wmtvar - msftwmtcov) / (msftvar + wmtvar - 2 * msftwmtcov)