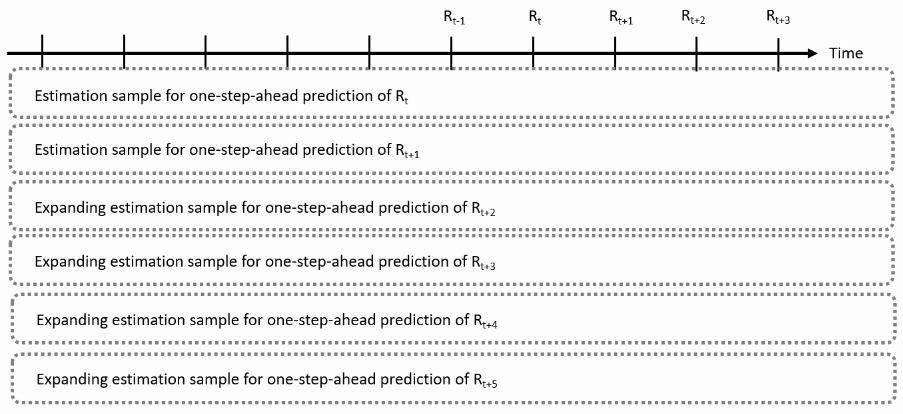

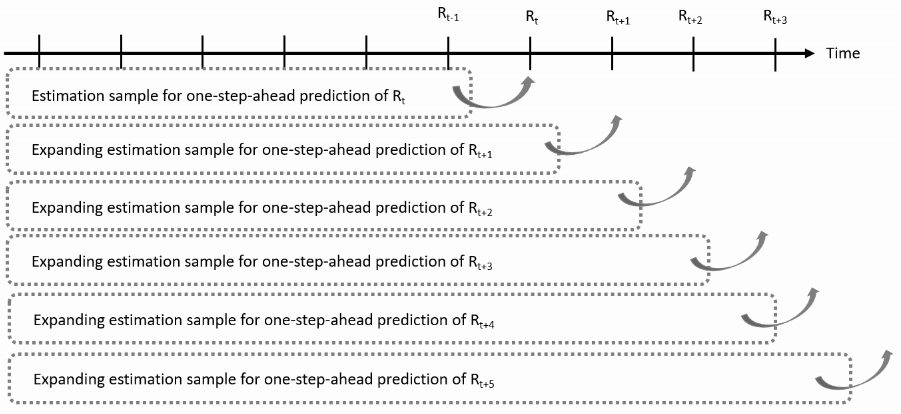

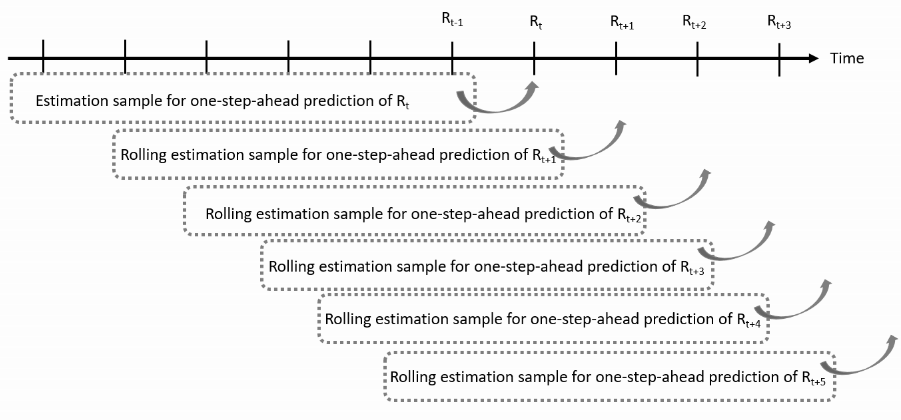

Use only the data that were available at the time of prediction

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

Volatility estimation by applying sigma() to ugarchfit object (ii)

Look ahead bias: Future returns are used to make the volatility estimate.

Expanding window estimation

Use all available returns at the time of prediction

Moving window estimation

Only use a fixed number of the most return observations available at the time of prediction

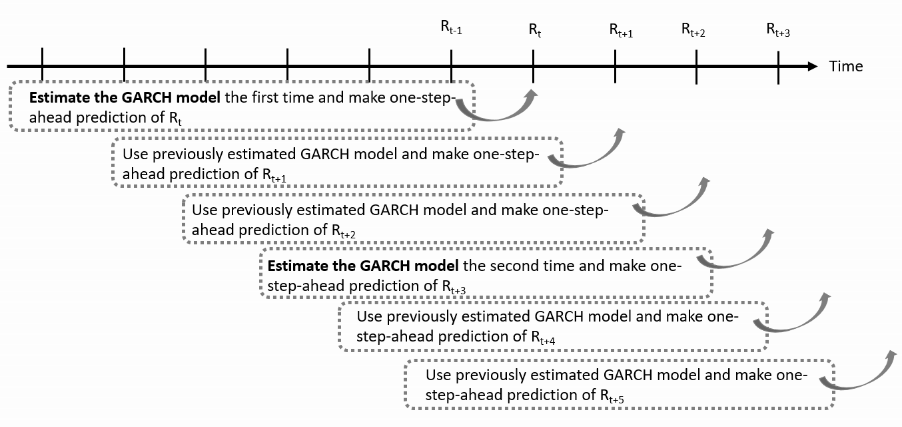

Rolling and re-estimation

Reduce the computational cost by estimating the model every $K$ observations

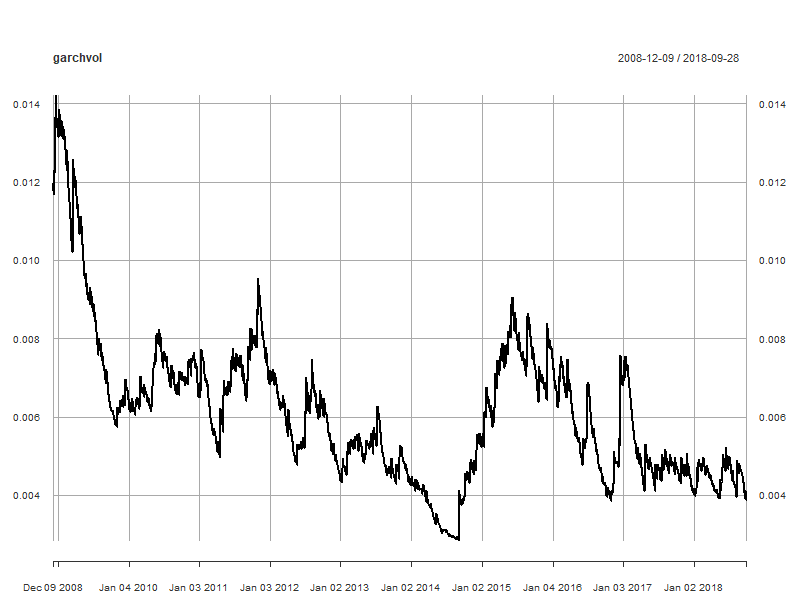

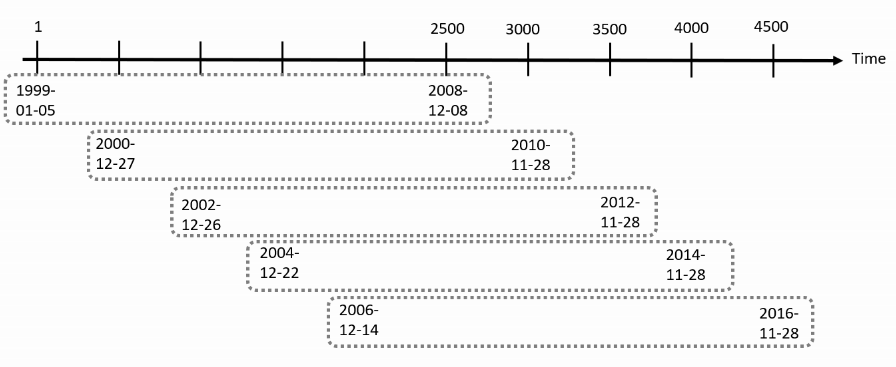

Example on the Jan 1999-Dec 2018 daily EUR/USD returns

For the 4961 EUR/USD returns with 4961 observations, starting on 1999-01-05 and using a moving estimation window of 2500 observations:

What is the rolling predicted mean and volatility?

For the EUR/USD returns with n.start = 2500, the first prediction is for observation 2501, namely 2008-12-09:

Predicted volatilities

garchvol <- xts(preds$Sigma, order.by = as.Date(rownames(preds)))

plot(garchvol)