Leverage effect

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

Illustration on MSFT returns

Estimate the model

garchfit <- ugarchfit(data = msftret, spec = garchspec)

Inspect the GARCH coefficients

coef(garchfit)[2:5]

omega alpha1 beta1 gamma1

2.007875e-06 3.423336e-02 9.363302e-01 5.531854e-02

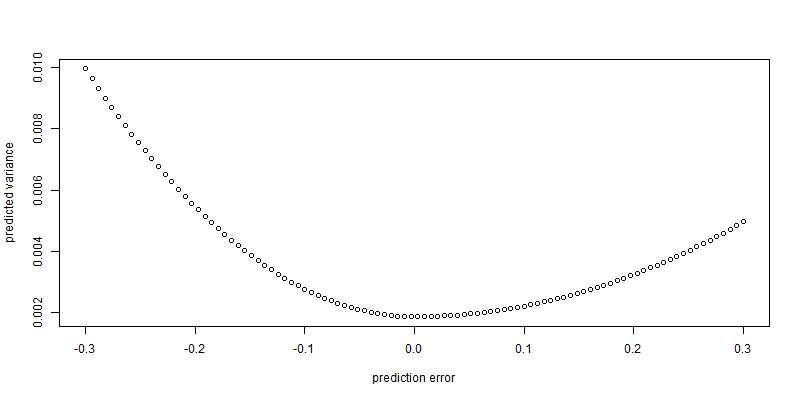

Visualize volatility response using newsimpact()

out <- newsimpact(garchfit)

plot(out$zx, out$zy, xlab = "prediction error", ylab = "predicted variance")