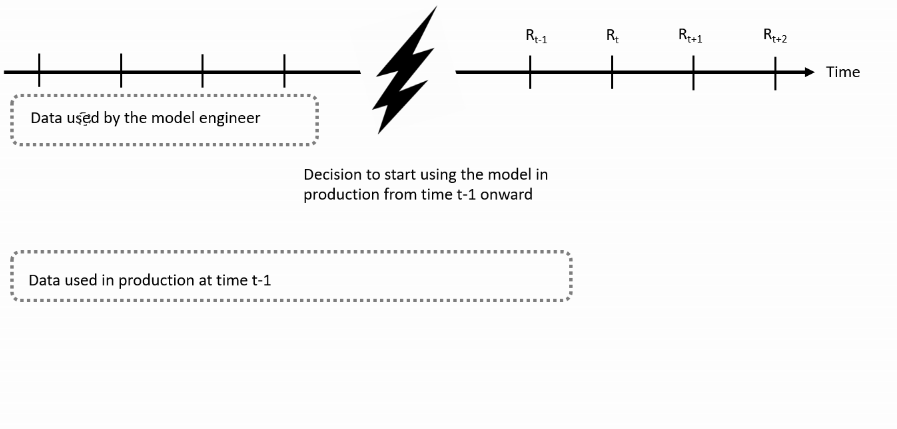

Use the validated GARCH model in production

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

Use in production

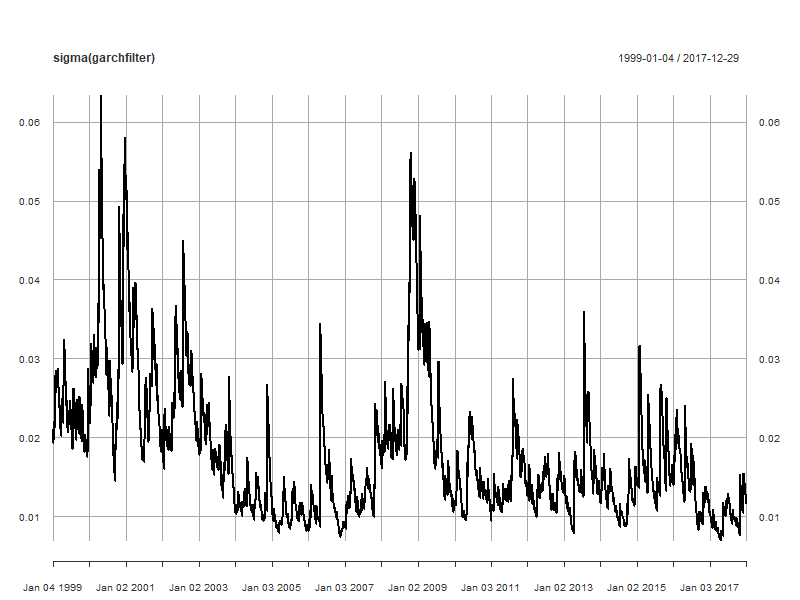

Step 2: Analysis of mean and volatility dynamics

Use the ugarchfilter() function:

garchfilter <- ugarchfilter(data = msftret, spec = progarchspec)

plot(sigma(garchfilter))

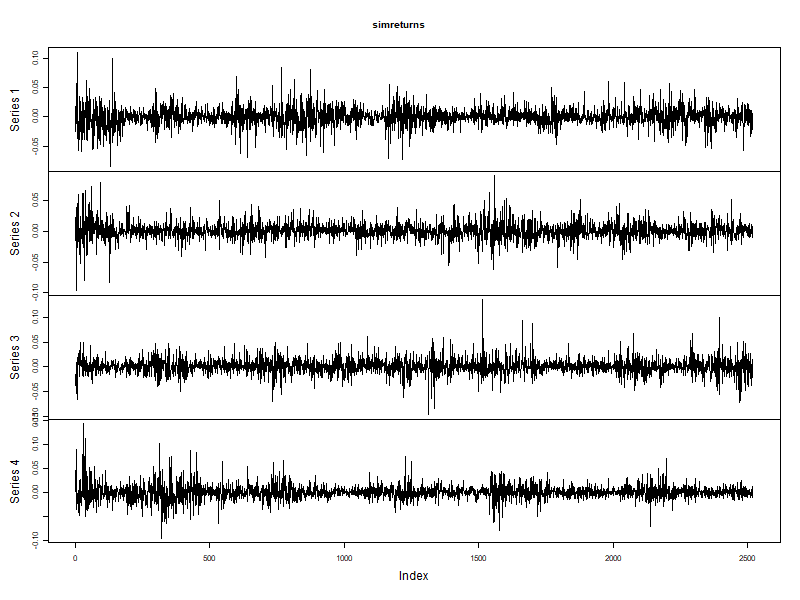

Step 3: Analysis of simulated returns

Method fitted() provides the simulated returns:

simret <- fitted(simgarch)

plot.zoo(simret)

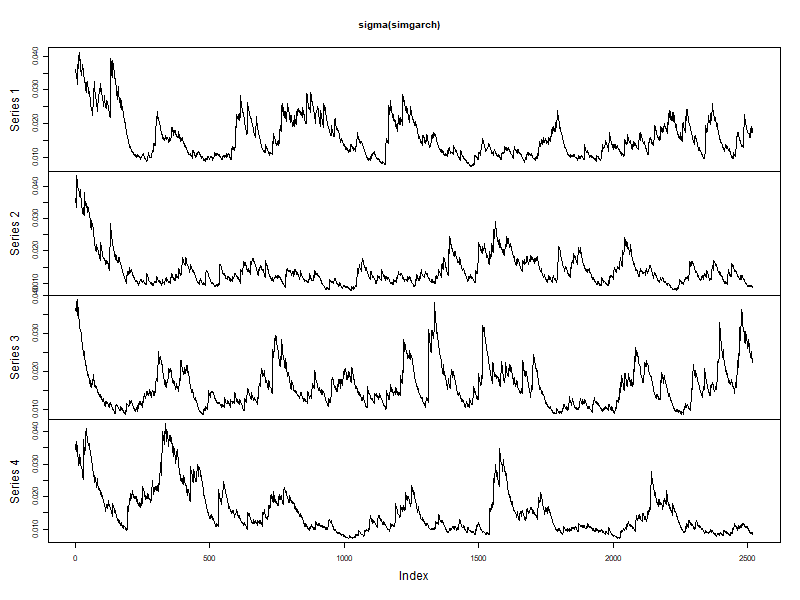

Analysis of simulated volatility

plot.zoo(sigma(simgarch))

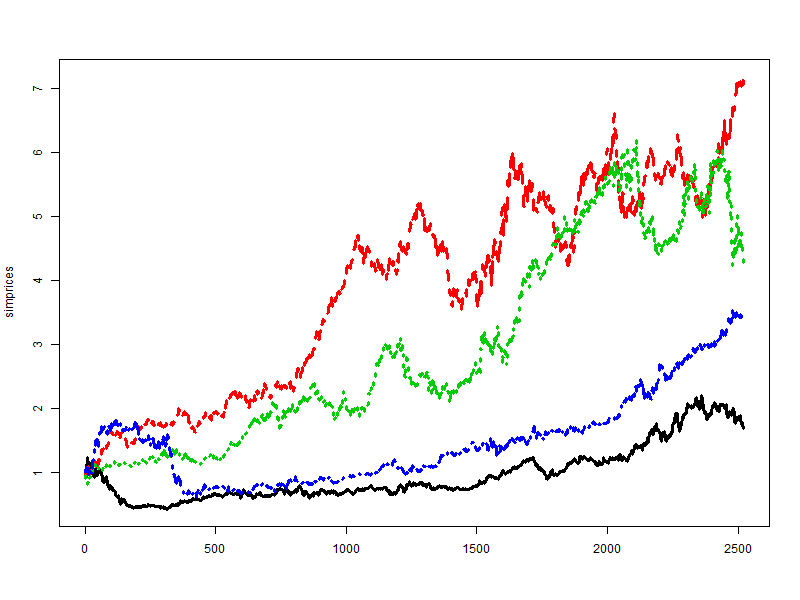

Analysis of simulated prices

Plotting 4 simulations of 10 years of stock prices, with initial price set at 1:

simprices <- exp(apply(simret, 2, "cumsum"))

matplot(simprices, type = "l", lwd = 3)