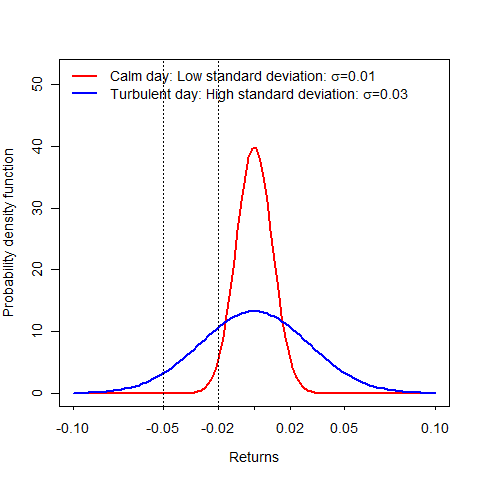

Analyzing volatility

GARCH Models in R

Kris Boudt

Professor of finance and econometrics

About the instructor

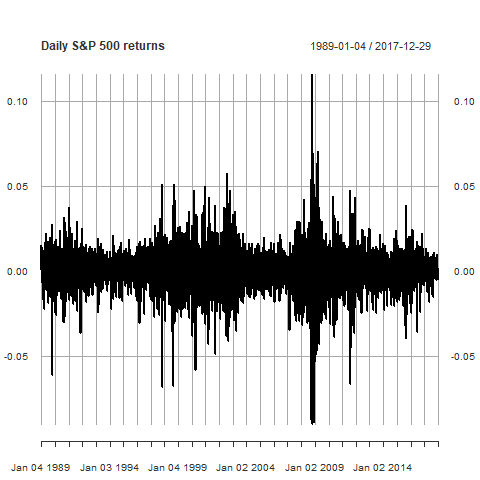

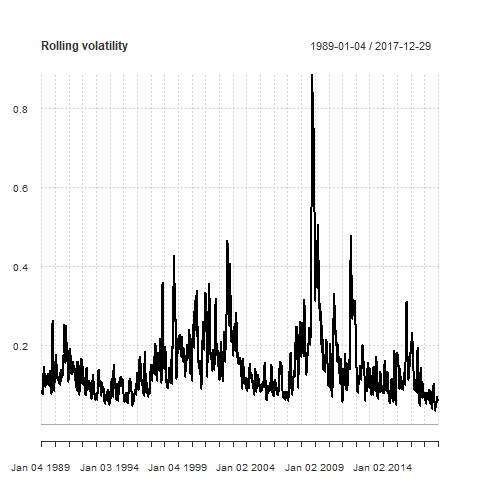

Daily S&P 500 returns

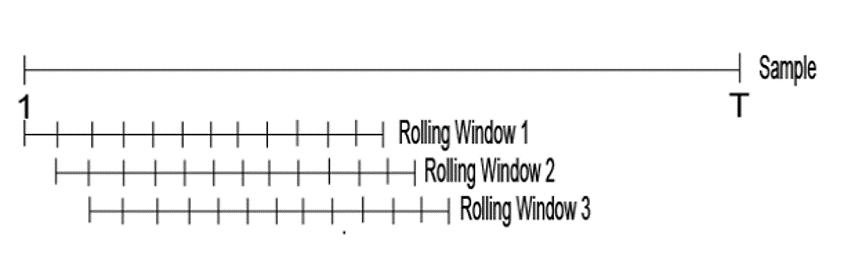

Rolling volatility estimation

- Rolling estimation windows :

- Window width? Multiple of 22 (trading days).

GARCH Models in R

Kris Boudt

Professor of finance and econometrics