Dimensions of portfolio performance

Introduction to Portfolio Analysis in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

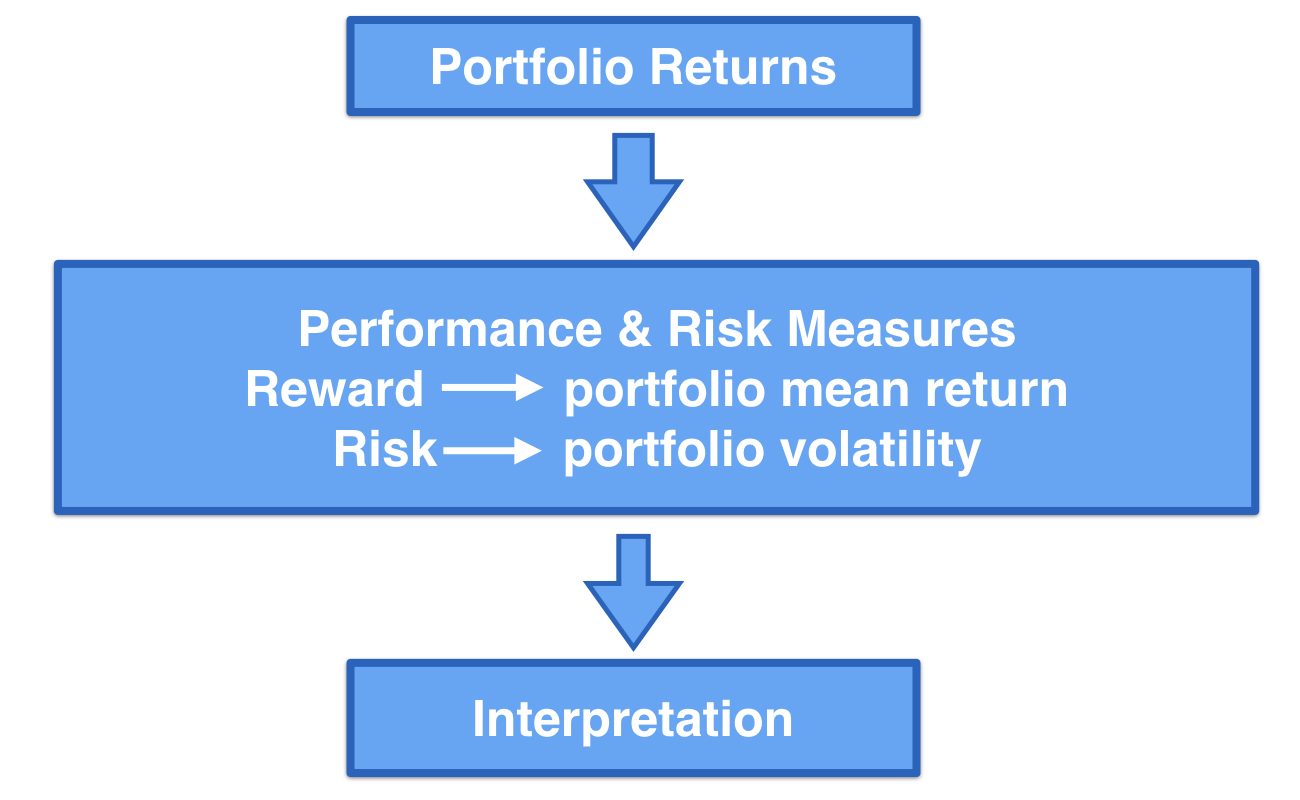

Interpretation of portfolio returns

Interpretation of portfolio returns

Interpretation of portfolio returns

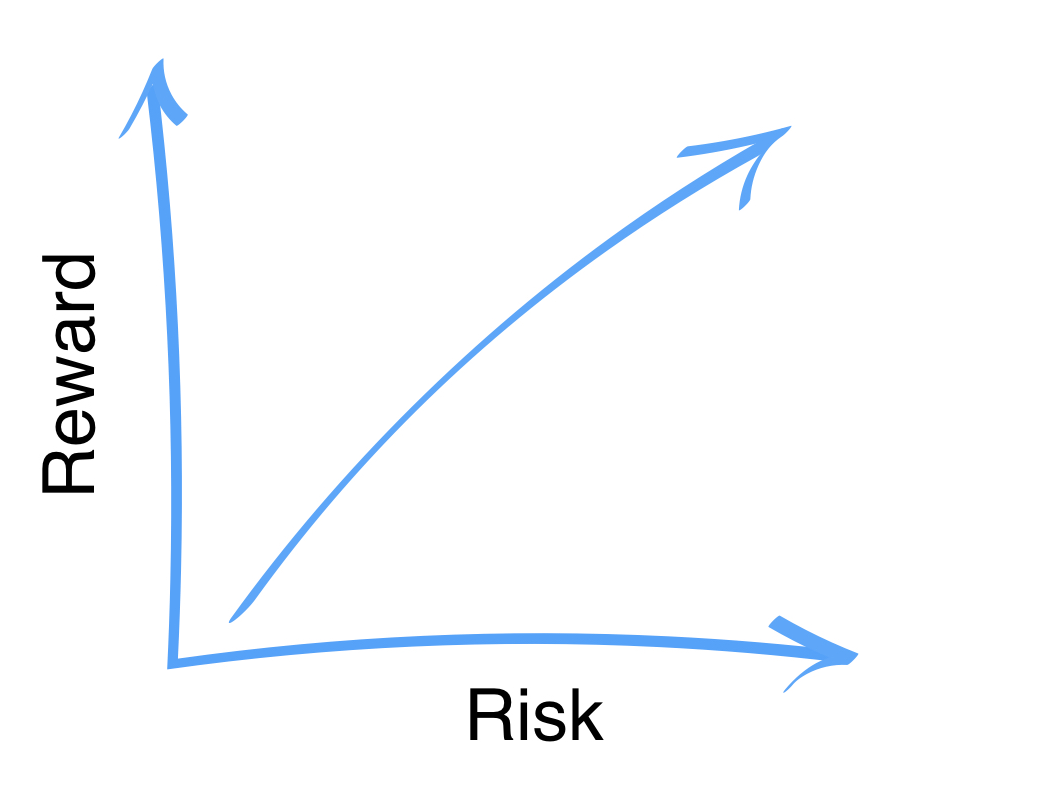

Risk vs. reward

Need for performance measure

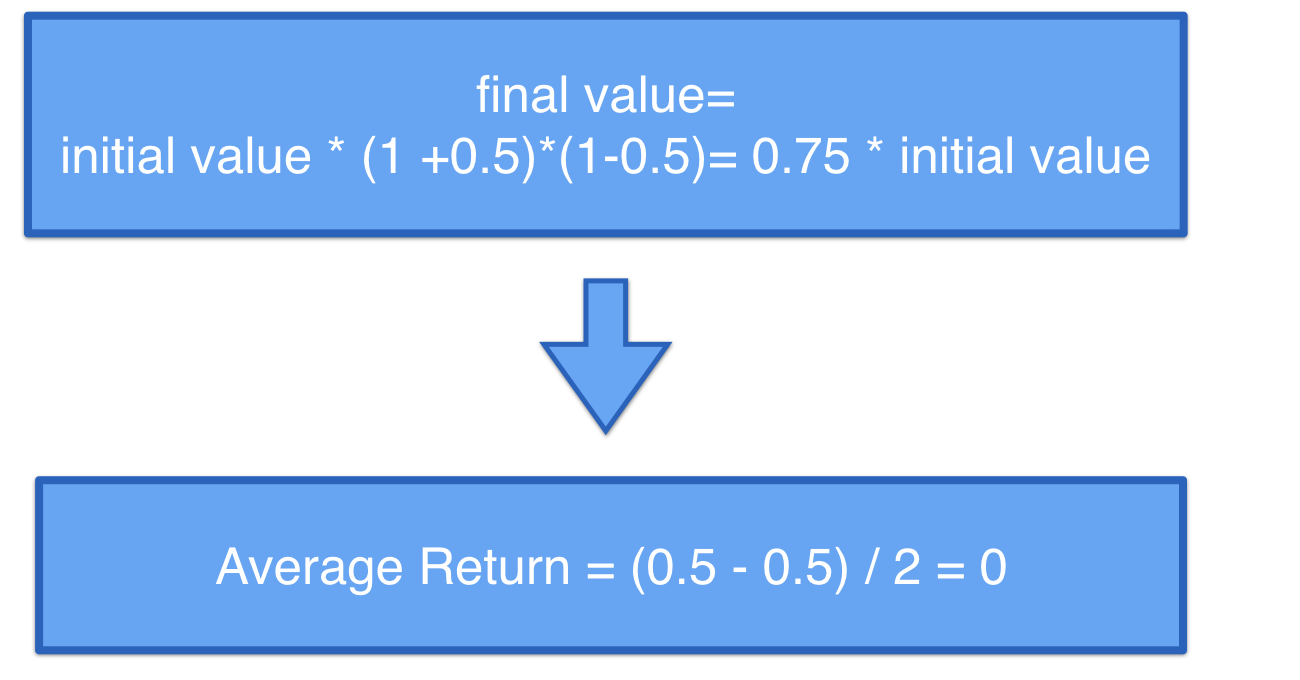

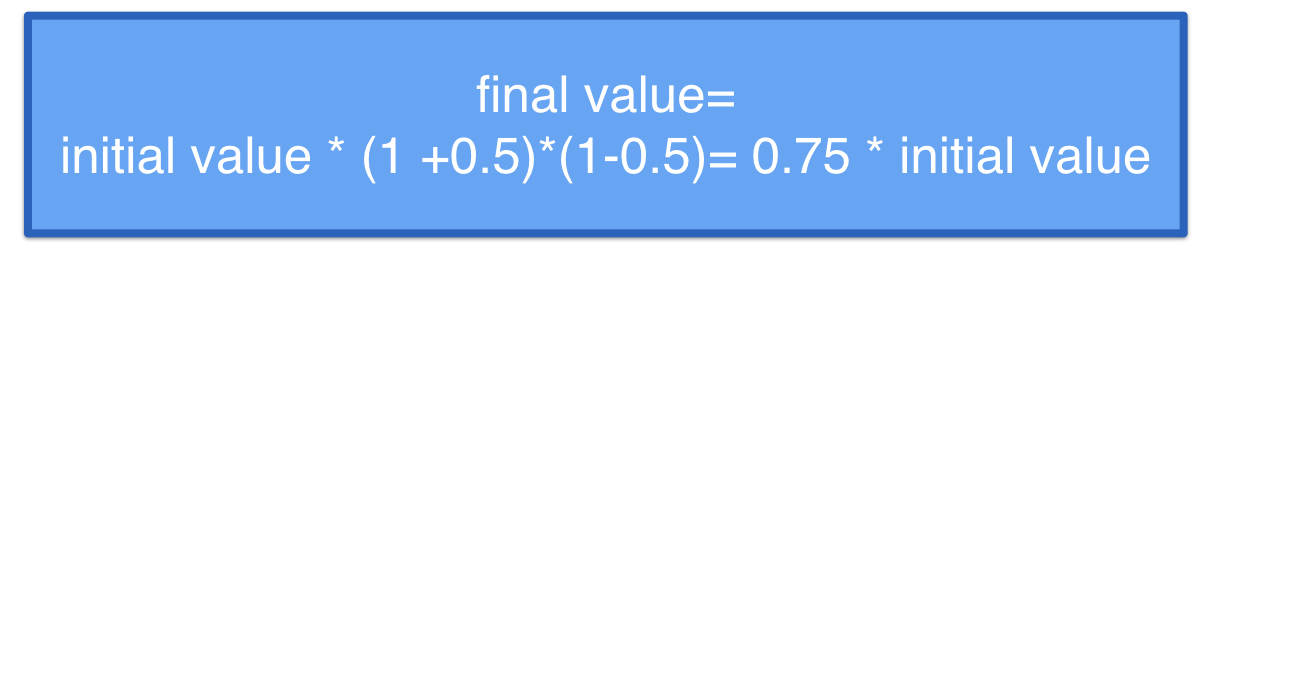

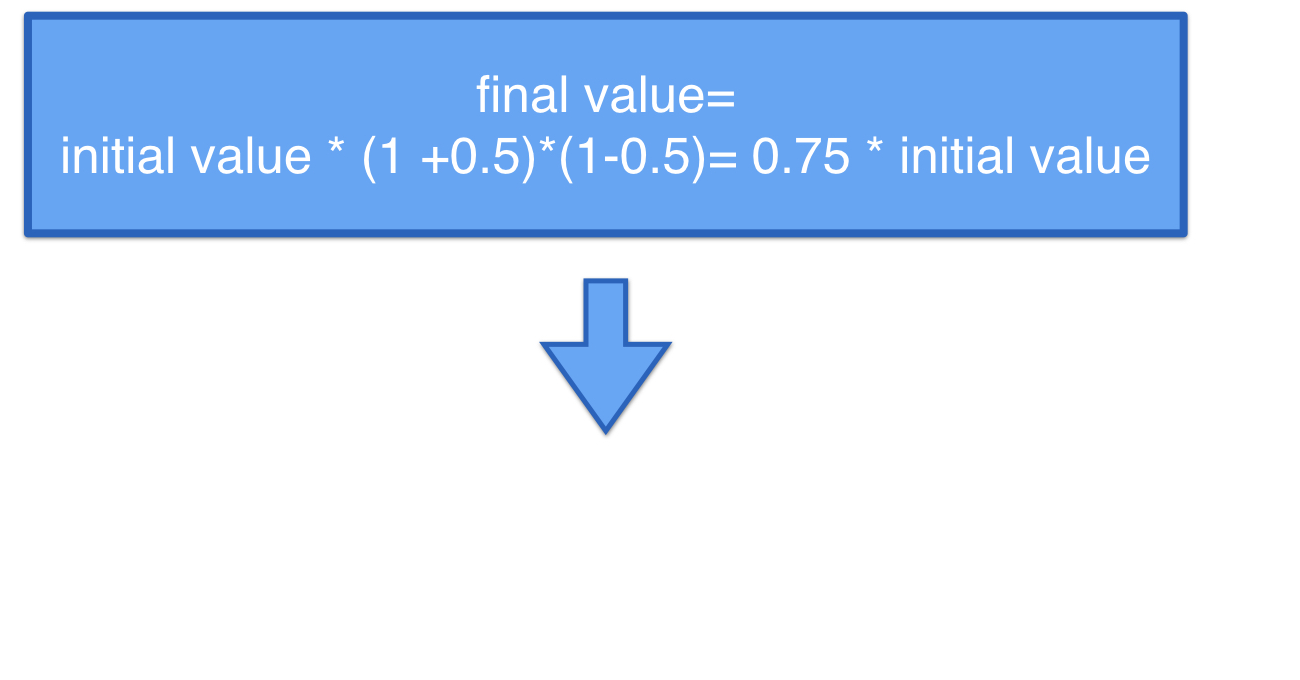

No linear compensation in return

- Mismatch between average return and effective return

No linear compensation in return

- Mismatch between average return and effective return

No linear compensation in return

- Mismatch between average return and effective return