Modern portfolio theory of Harry Markowitz

Introduction to Portfolio Analysis in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

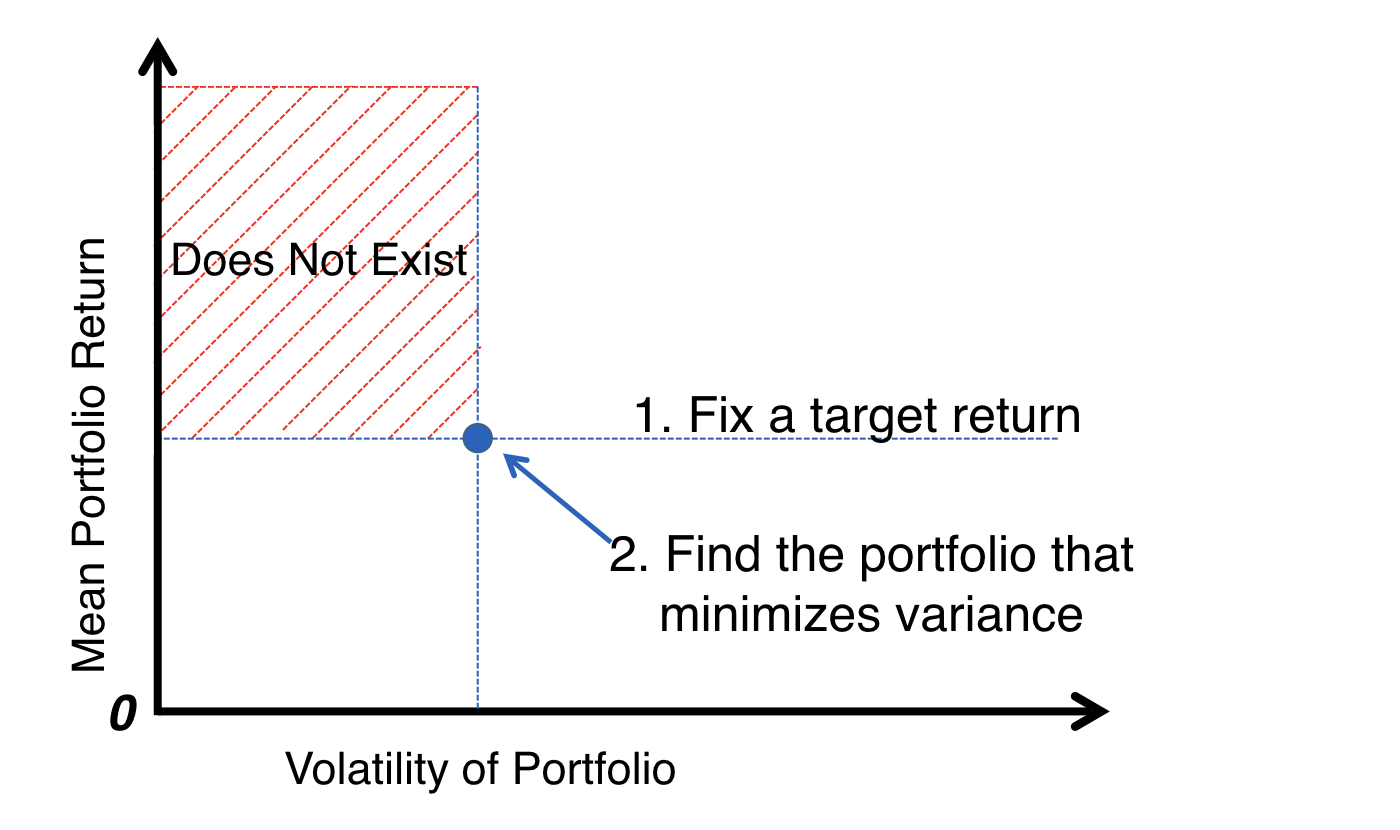

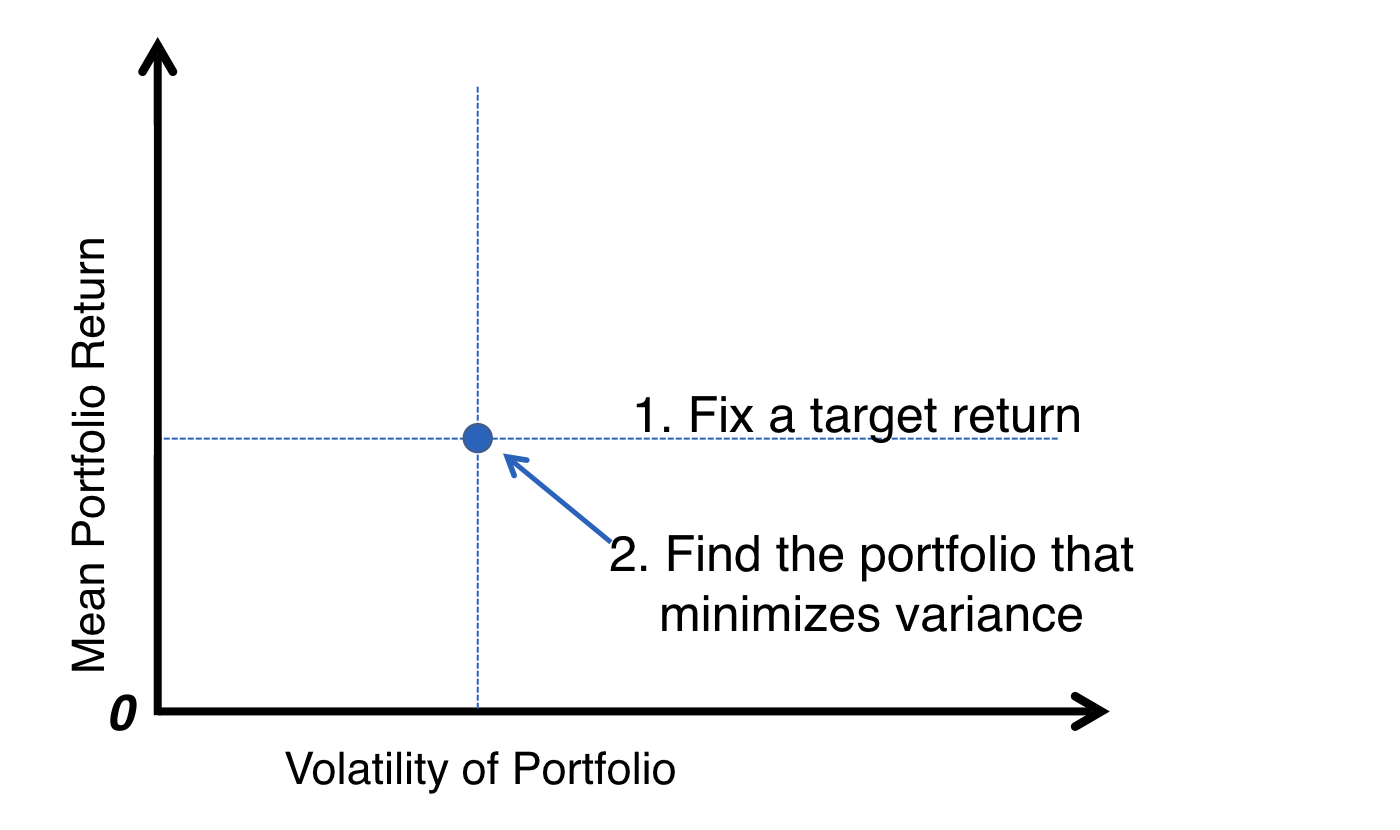

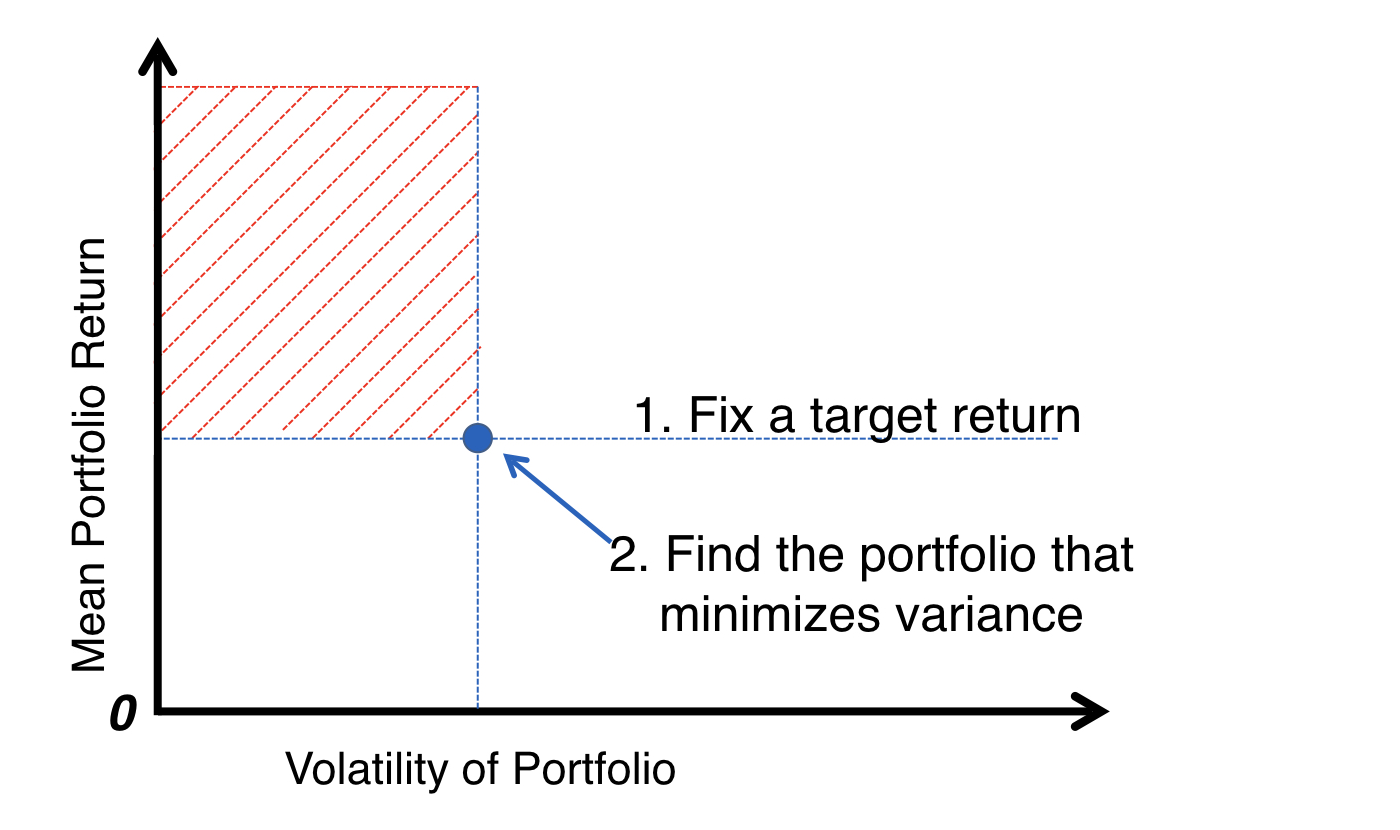

The H. Markowitz approach

The H. Markowitz approach

The H. Markowitz approach

The H. Markowitz approach

The H. Markowitz approach