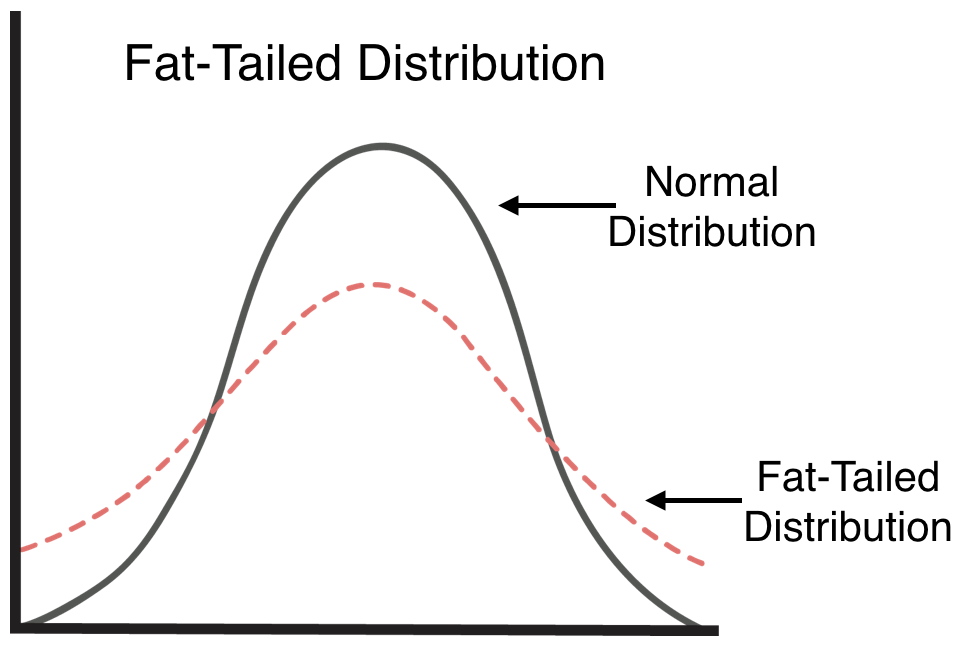

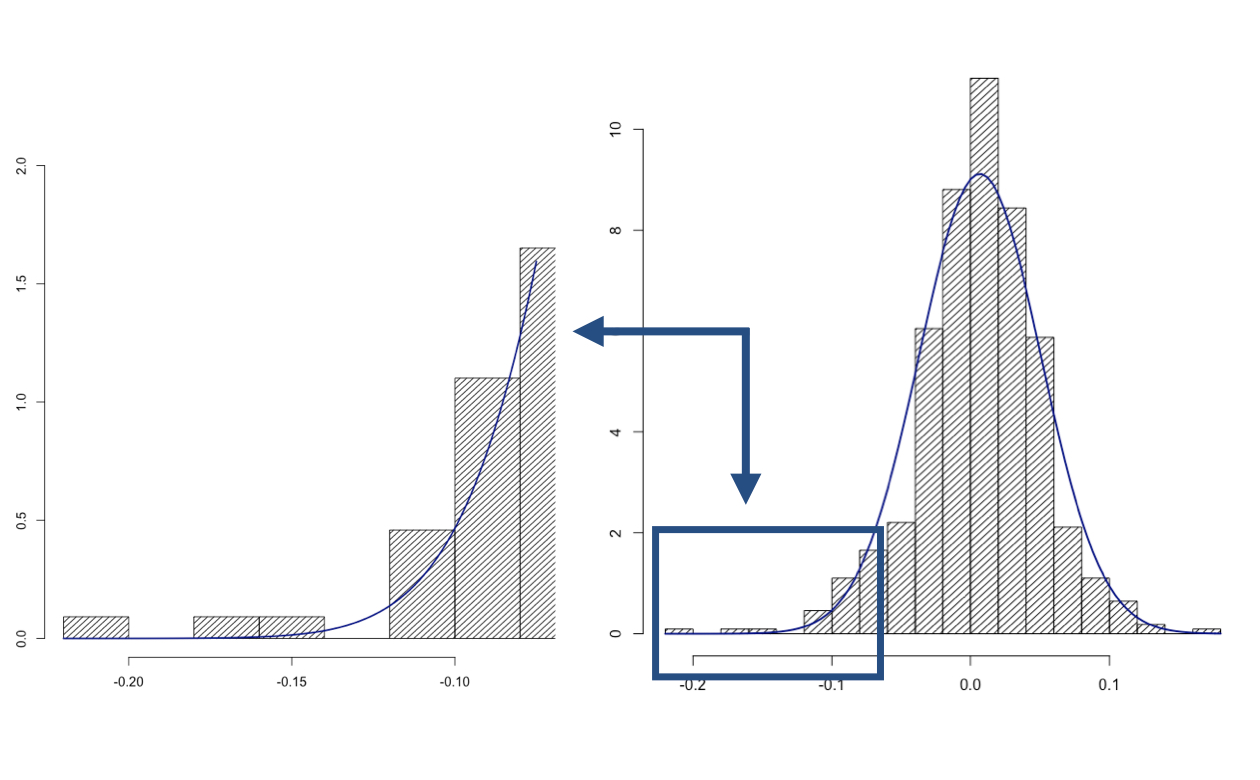

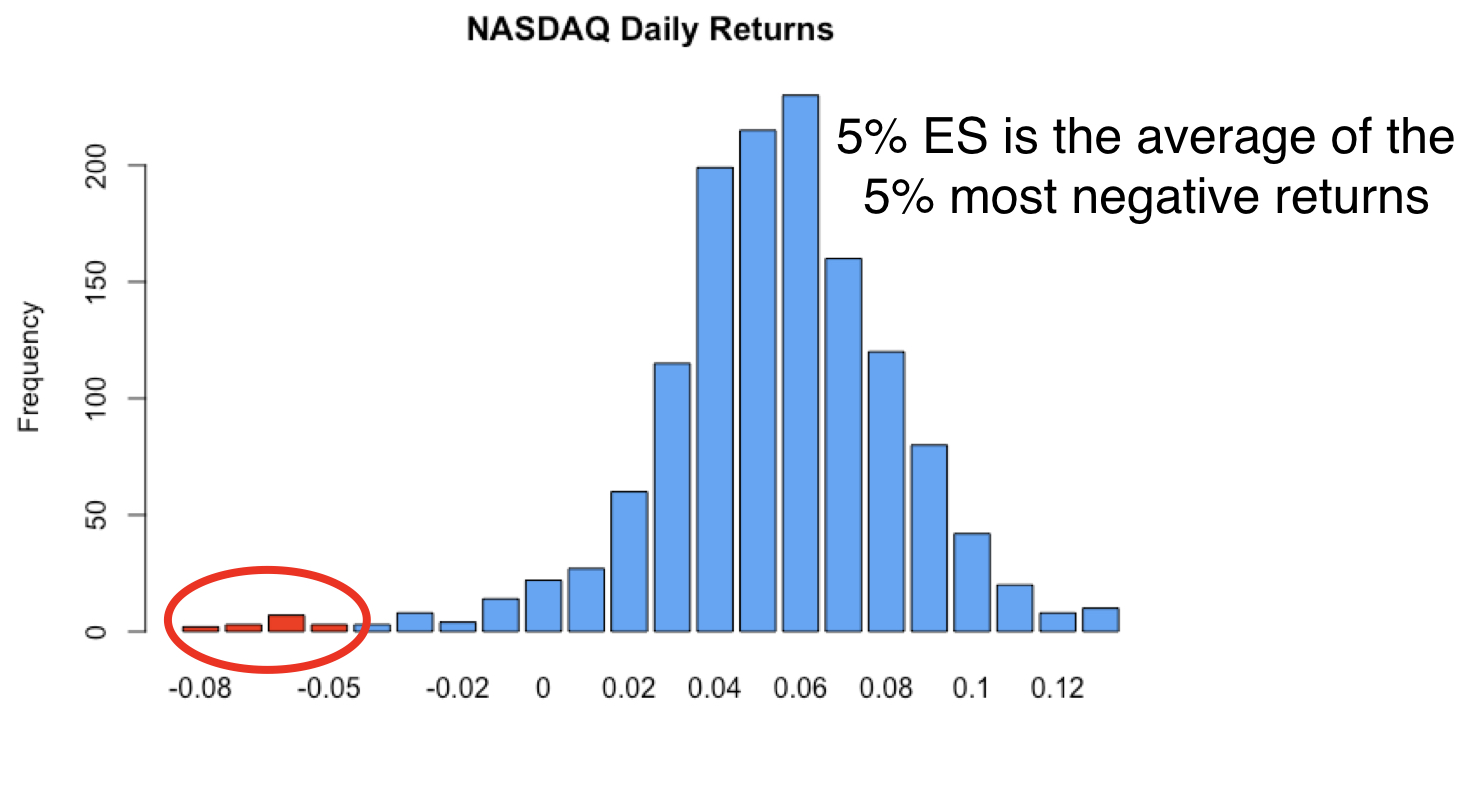

Non-normality of the return distribution

Introduction to Portfolio Analysis in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

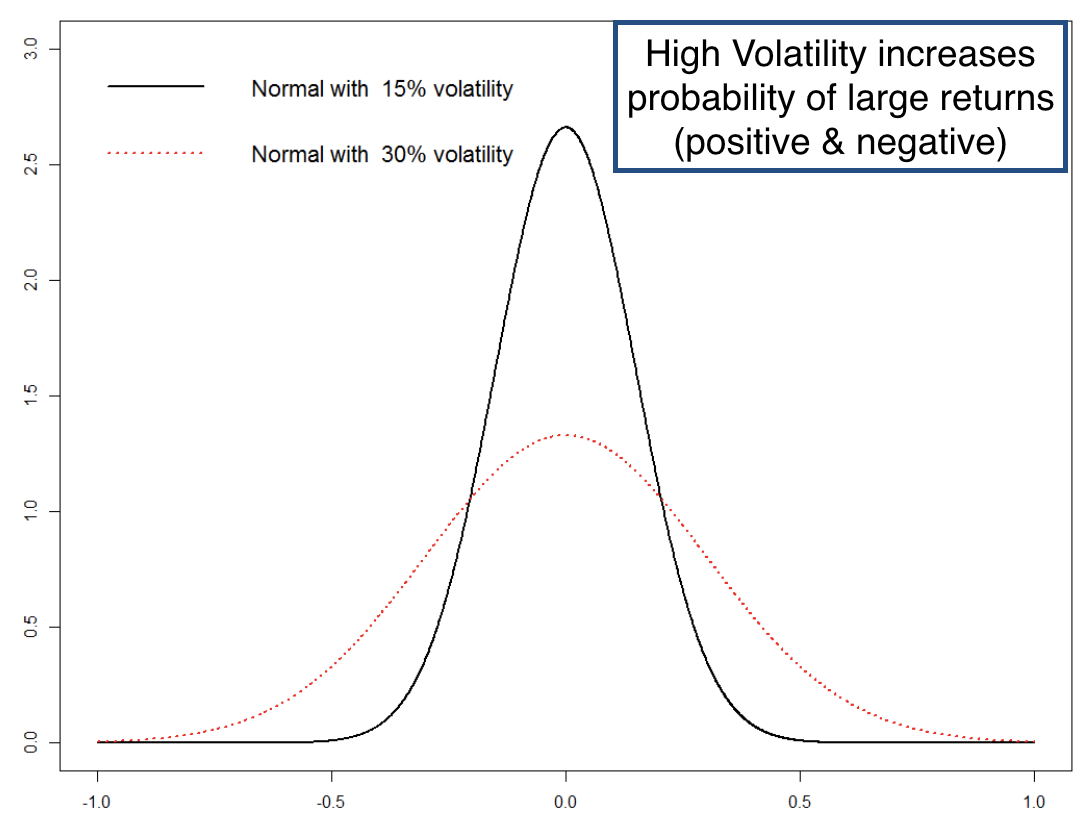

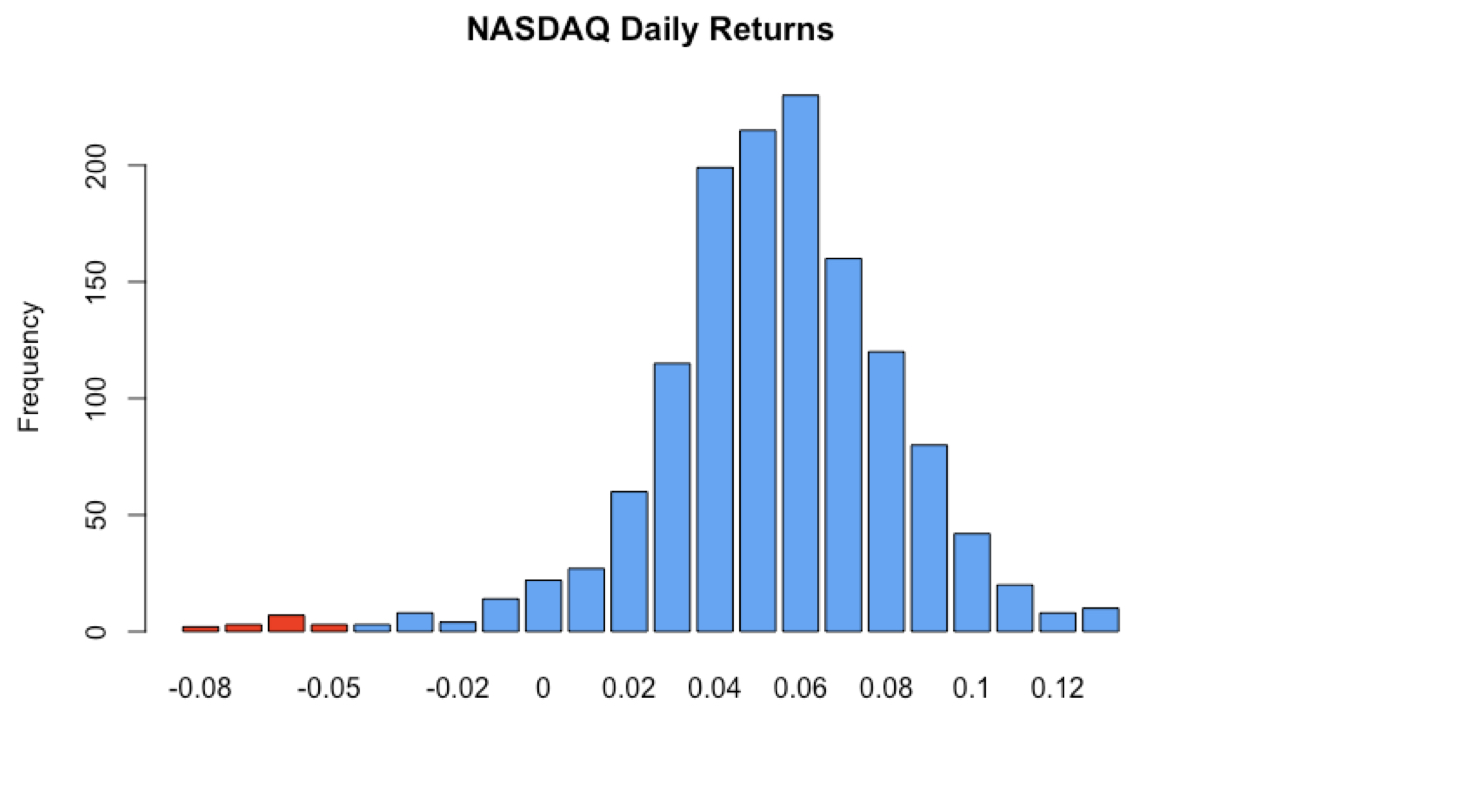

Volatility describes "normal" risk

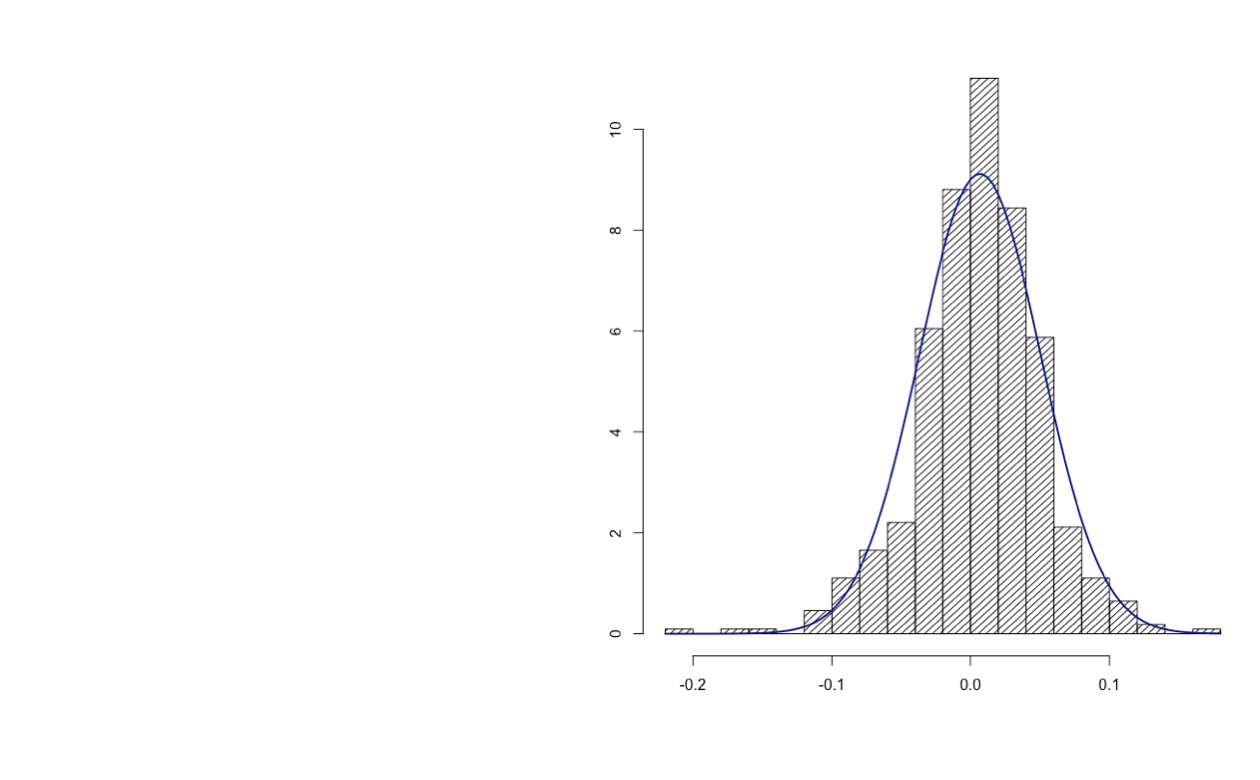

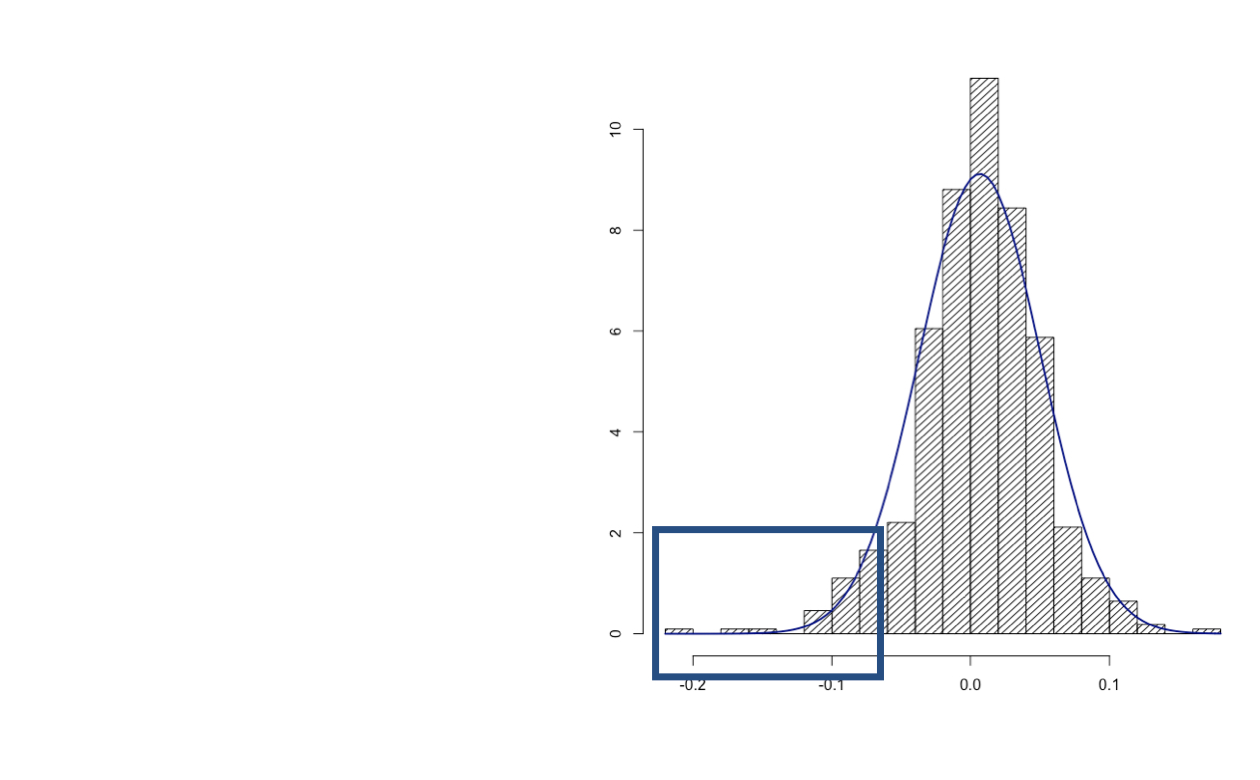

Non-normality of return

Non-normality of return

Non-normality of return

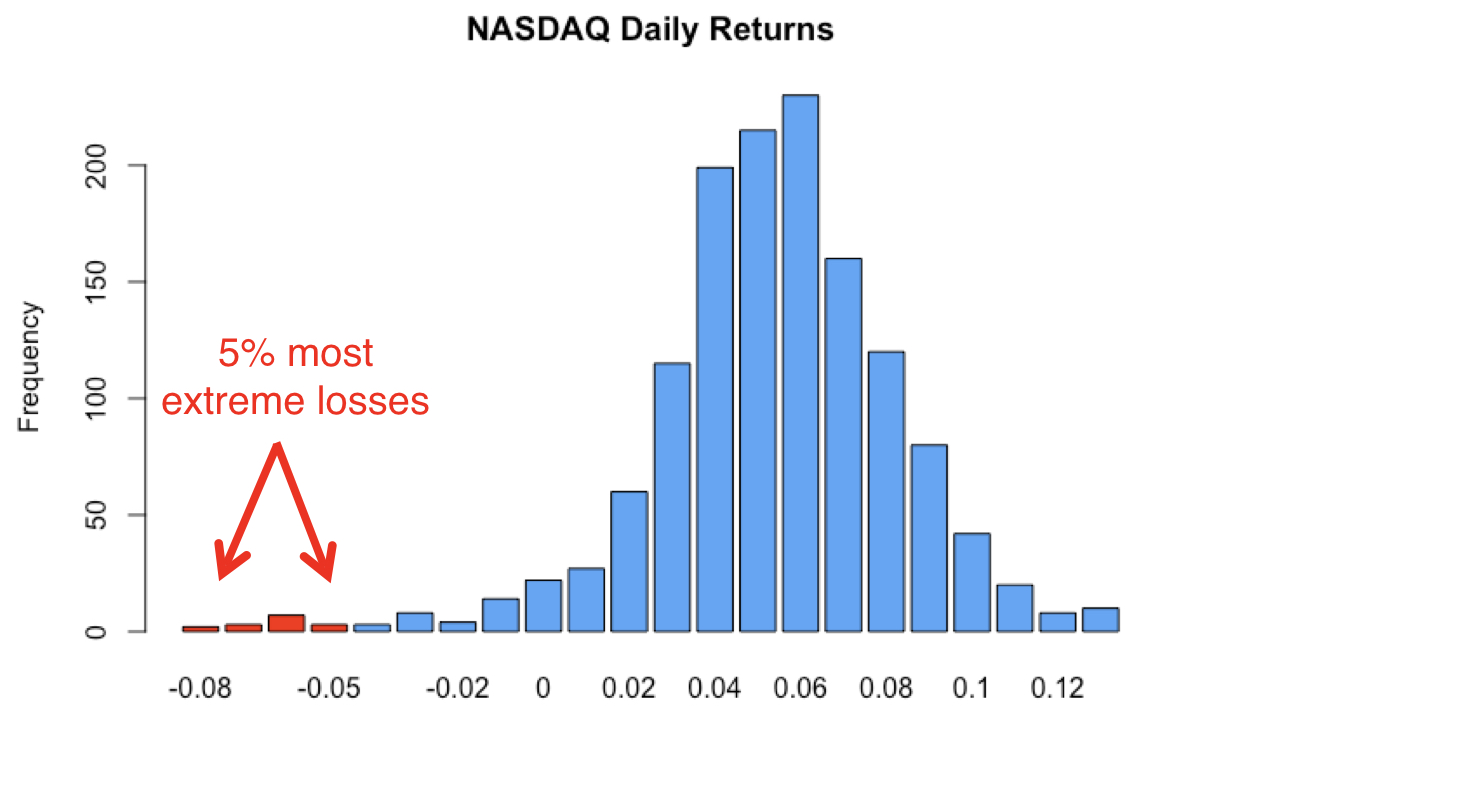

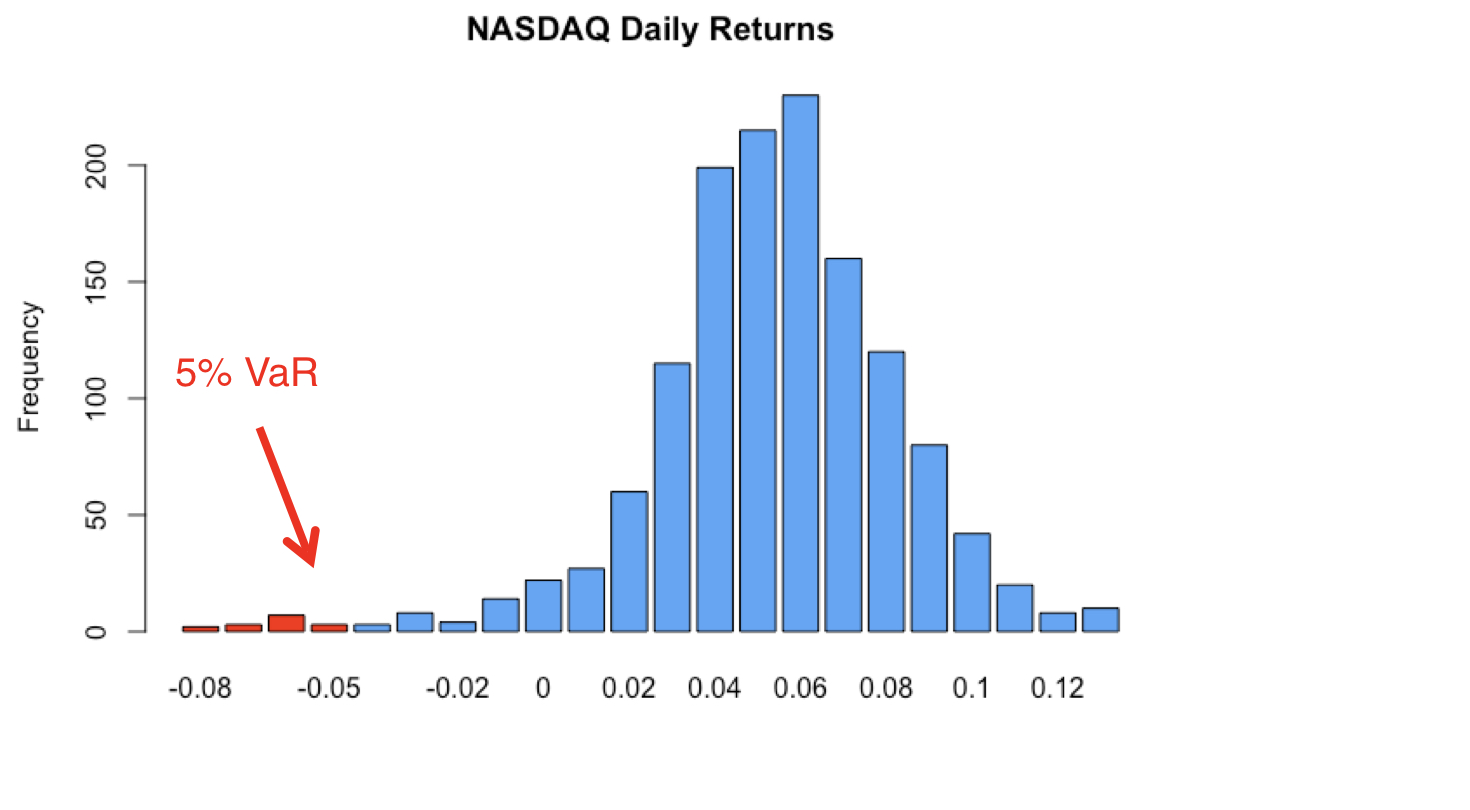

Value-at-risk & expected shortfall

Value-at-risk & expected shortfall

Value-at-risk & expected shortfall

Value-at-risk & expected shortfall

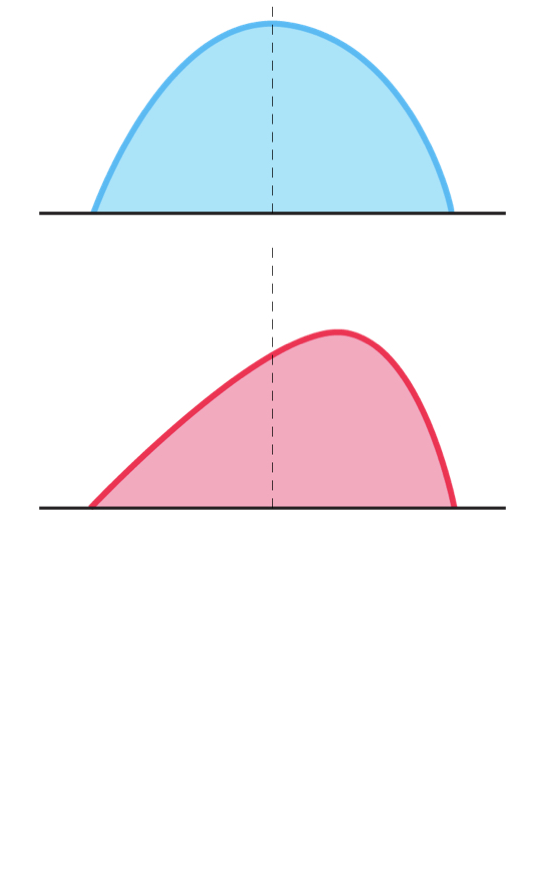

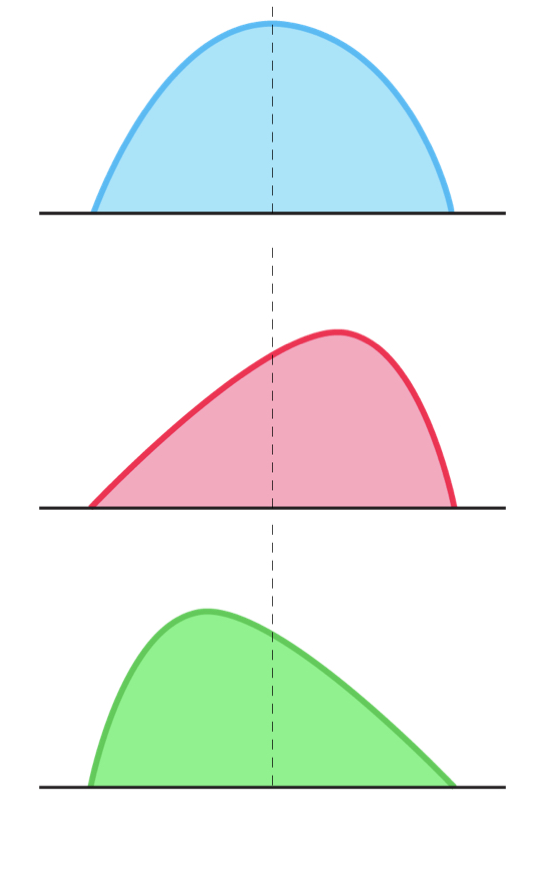

Skewness

Skewness

Skewness

Kurtosis

- The distribution is fat-tailed when the excess kurtosis > 0