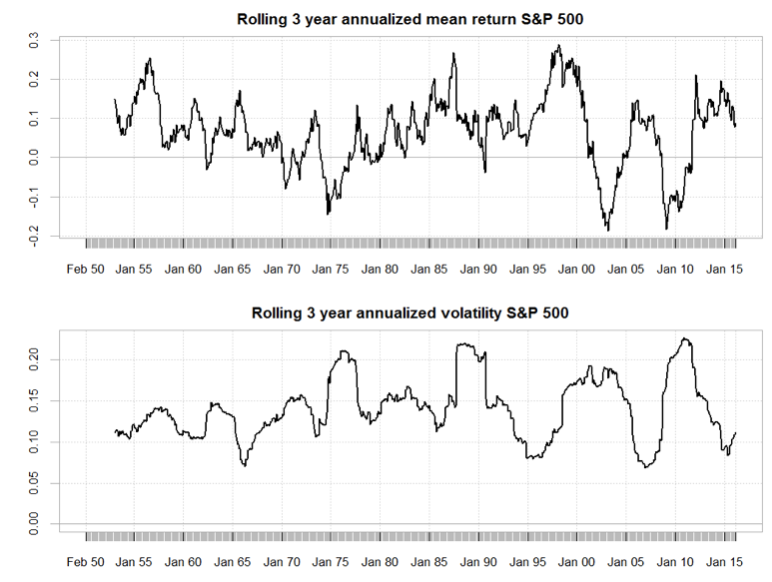

Time-variation in portfolio performance

Introduction to Portfolio Analysis in R

Kris Boudt

Professor, Free University Brussels & Amsterdam

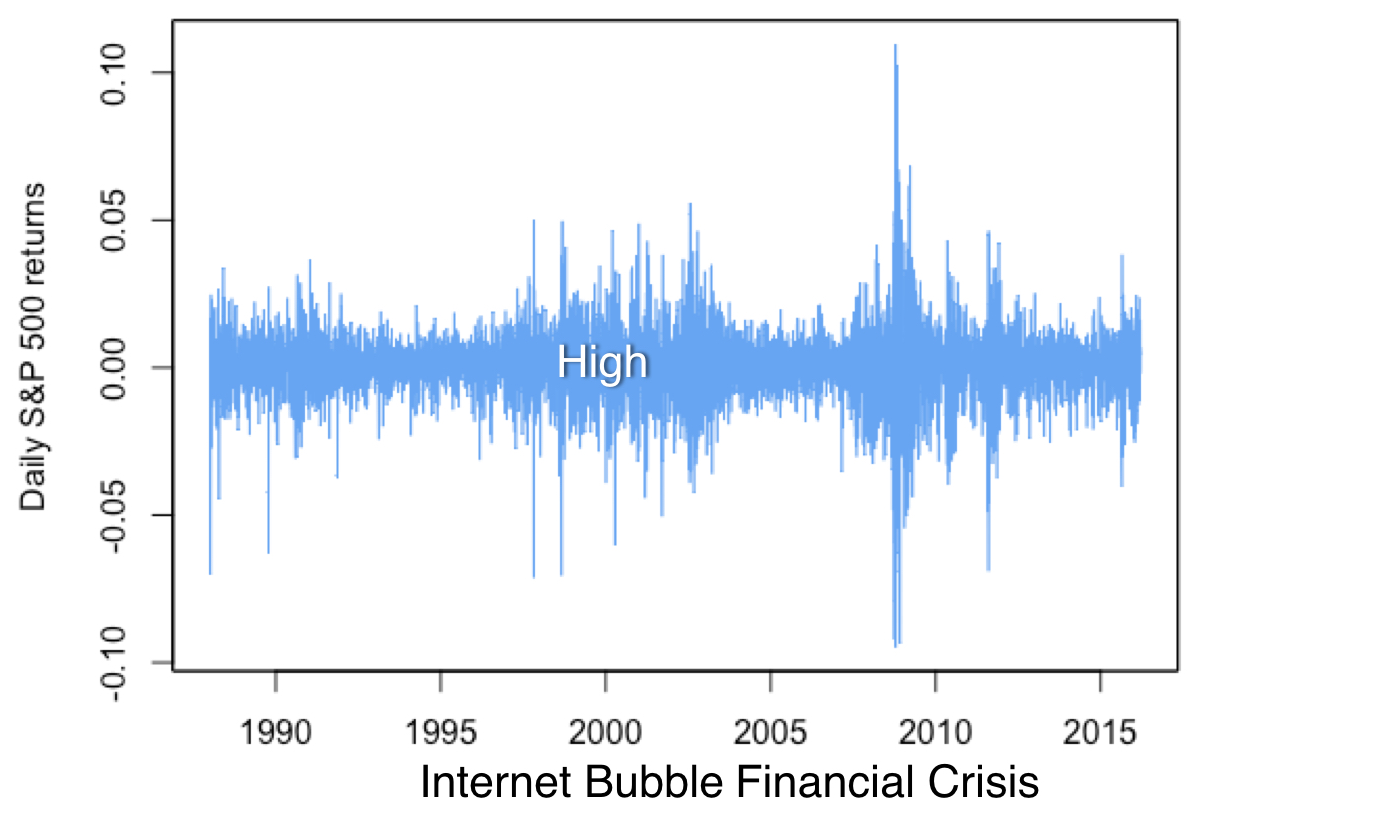

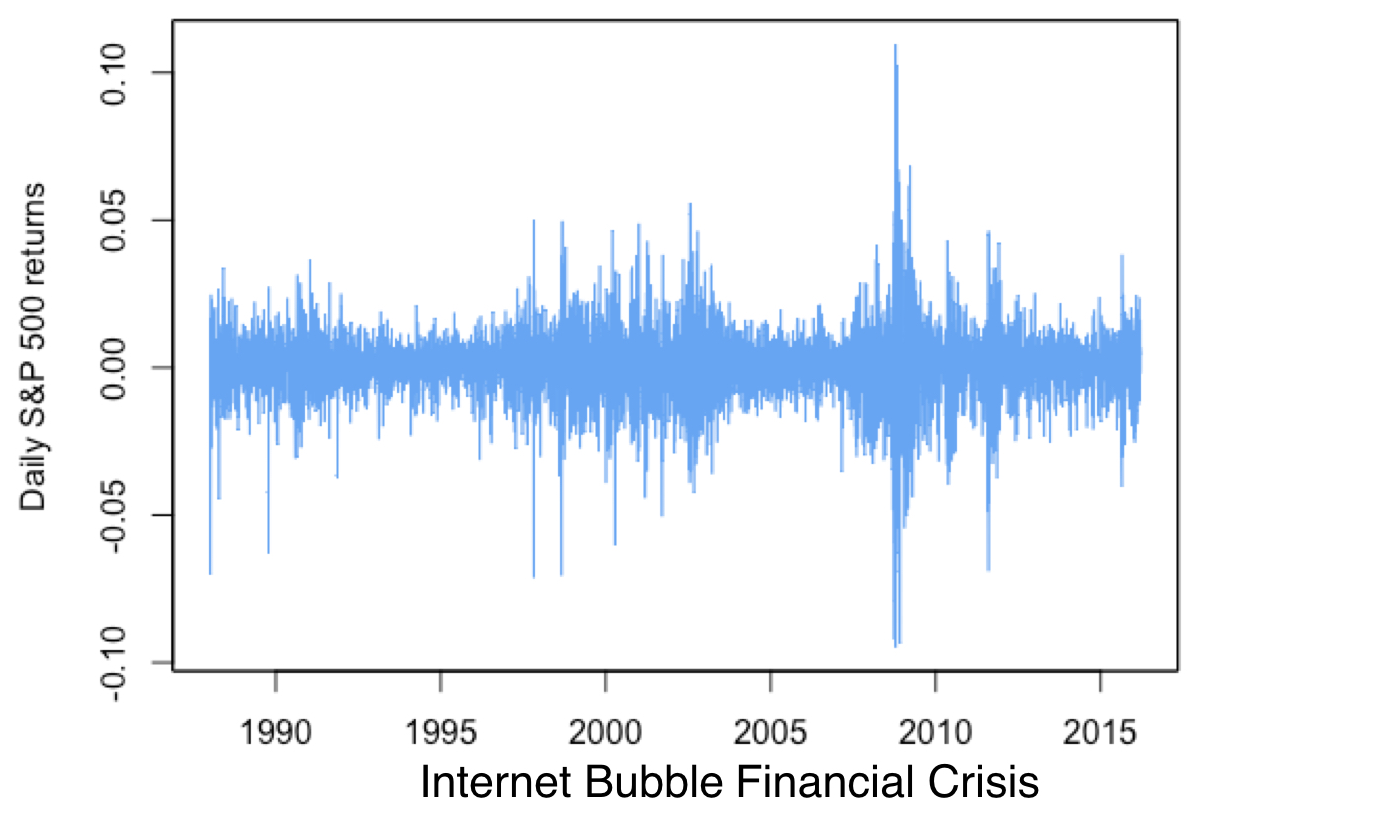

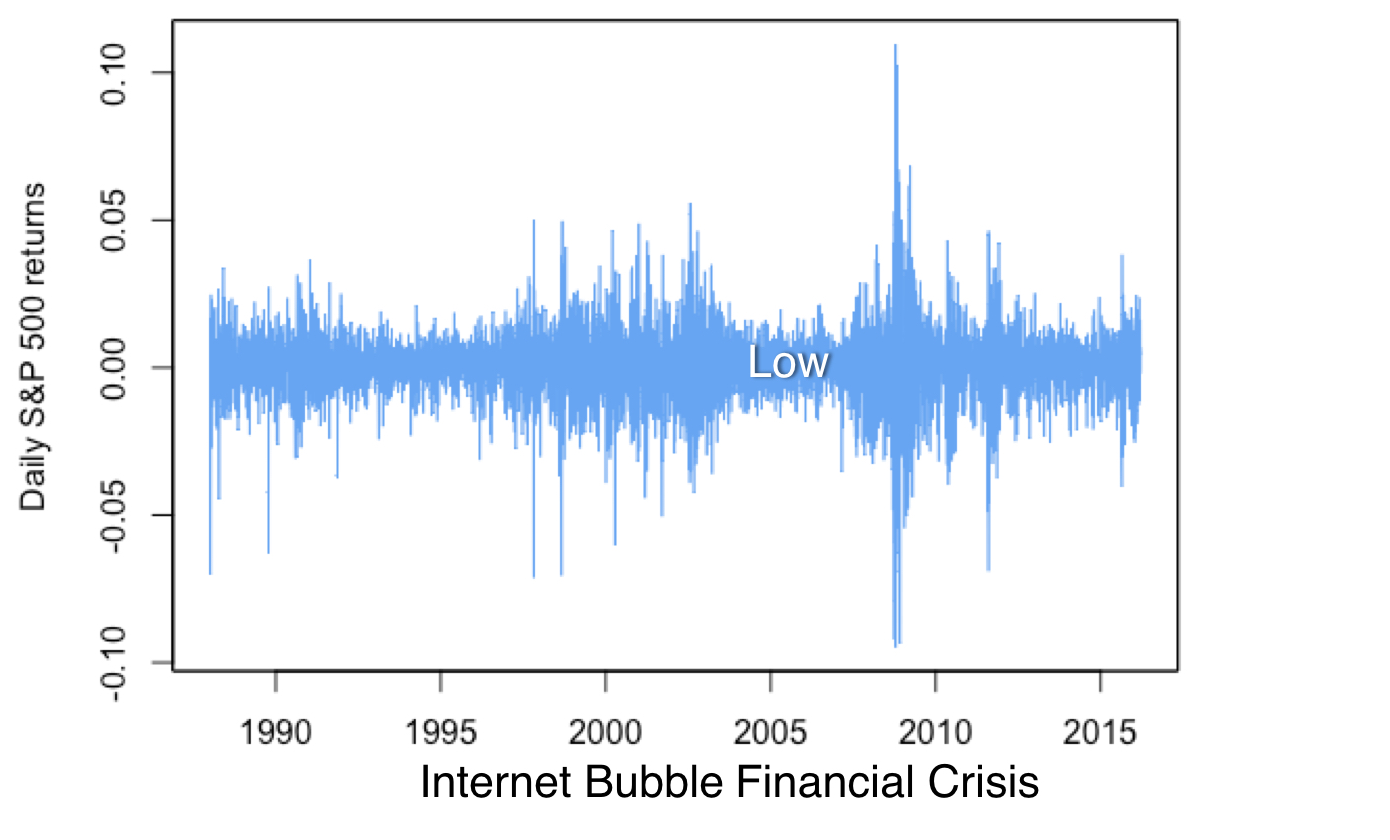

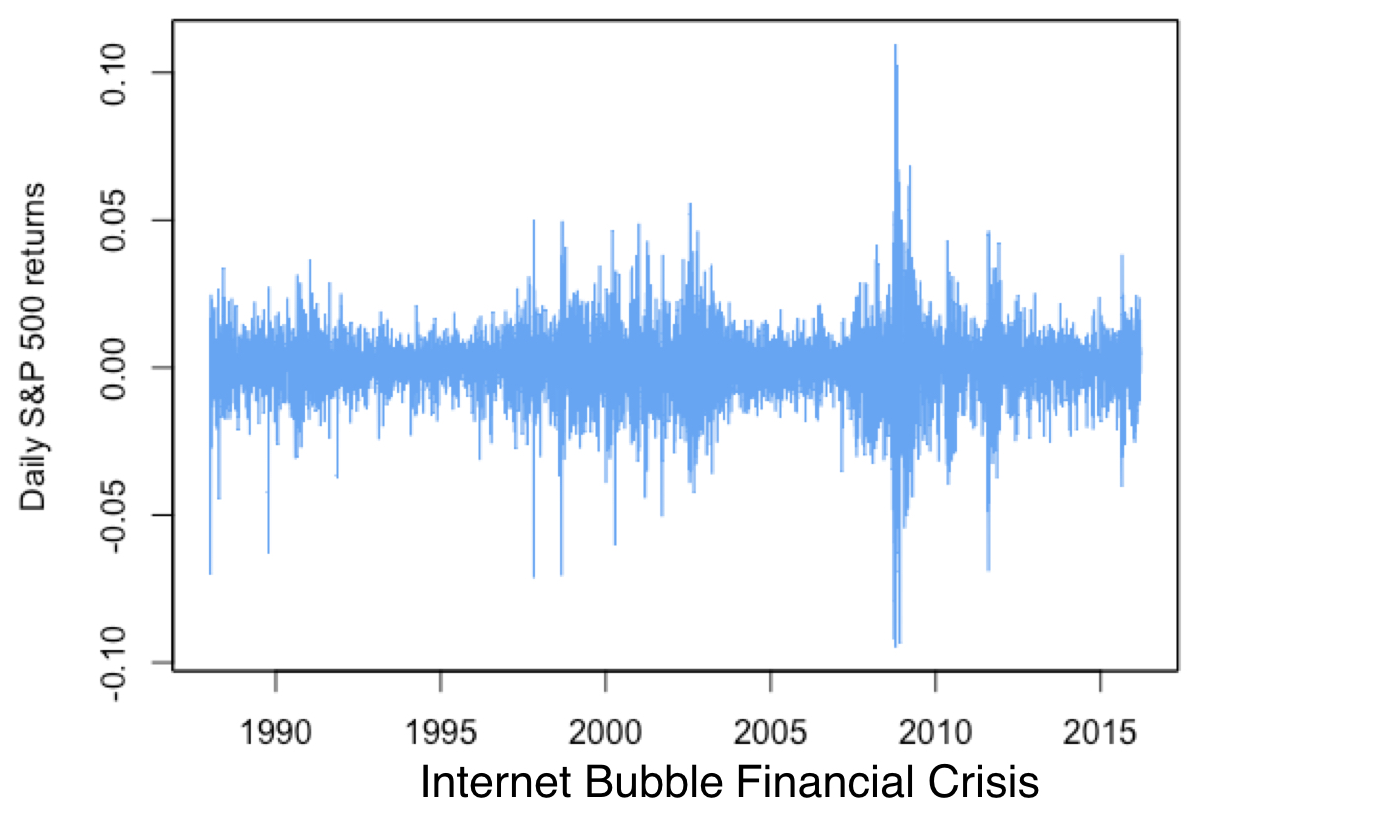

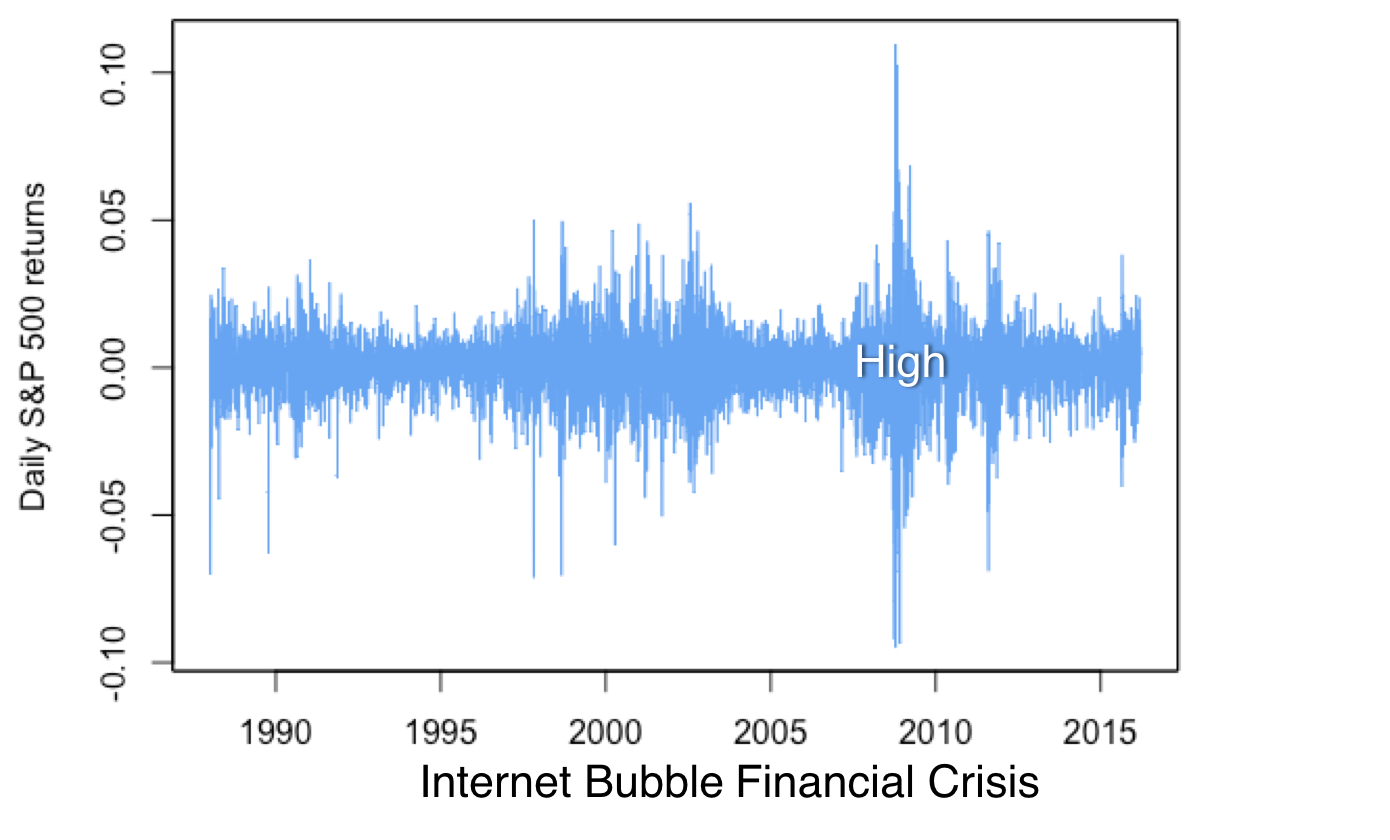

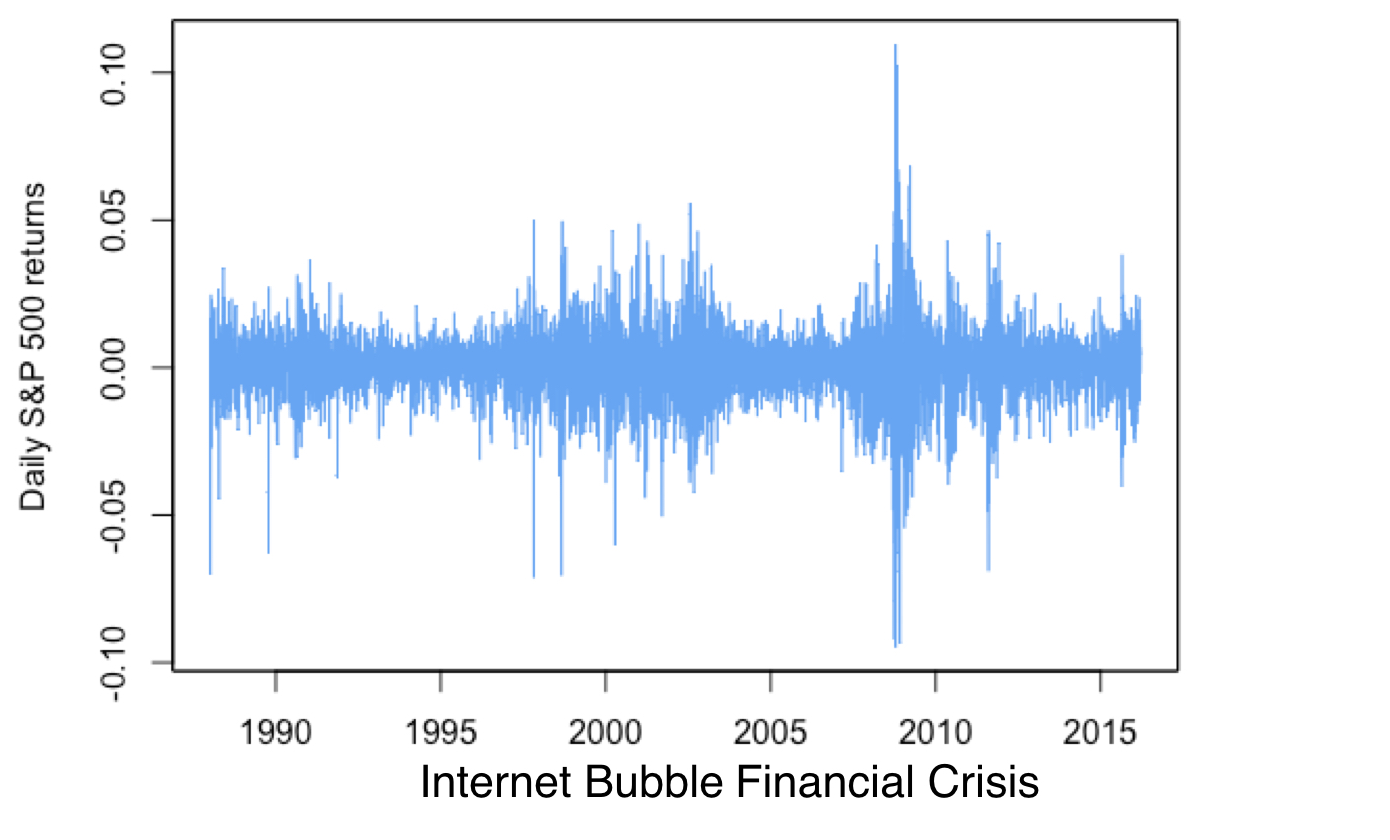

Bulls & bears

- Business cycle, news, and swings in the market psychology affect the market

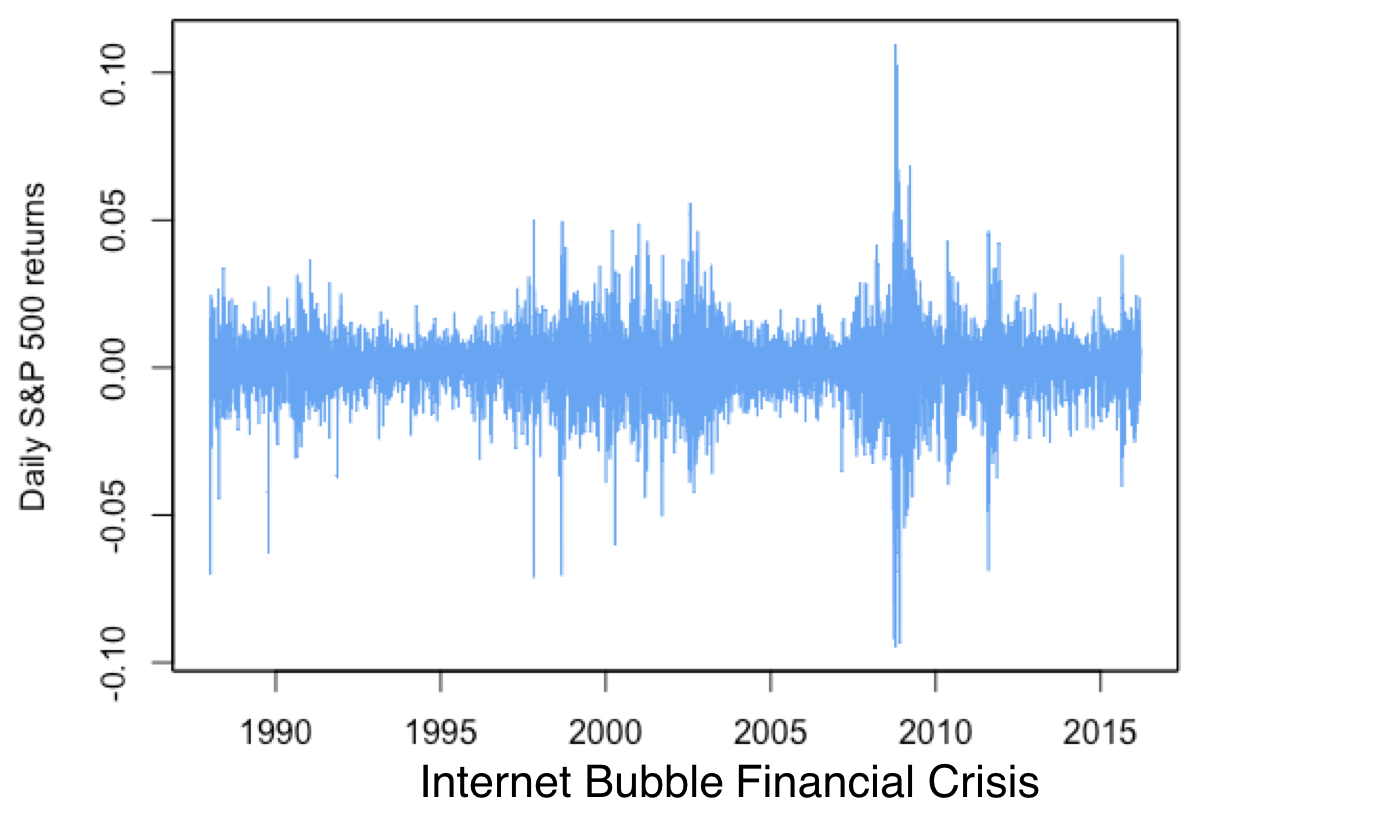

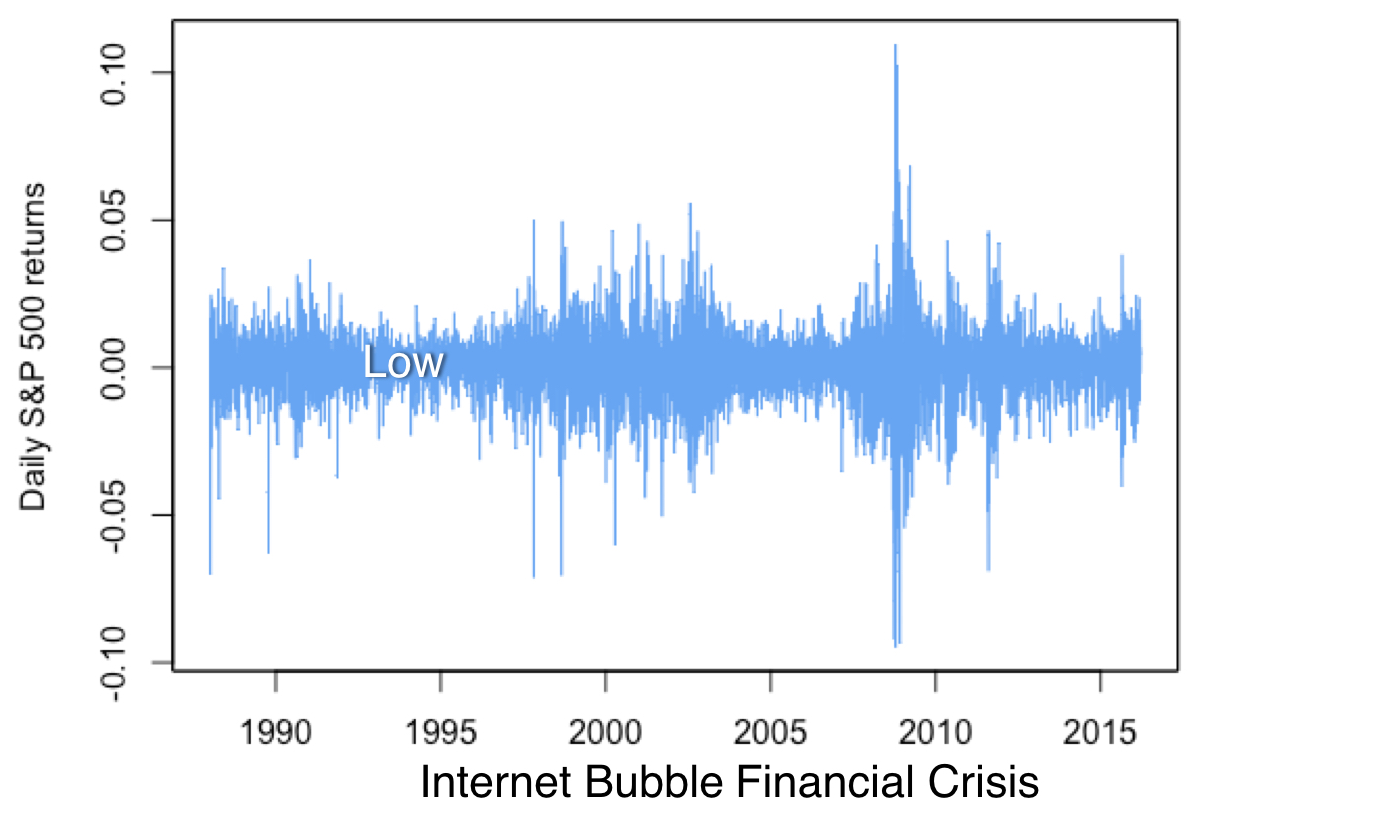

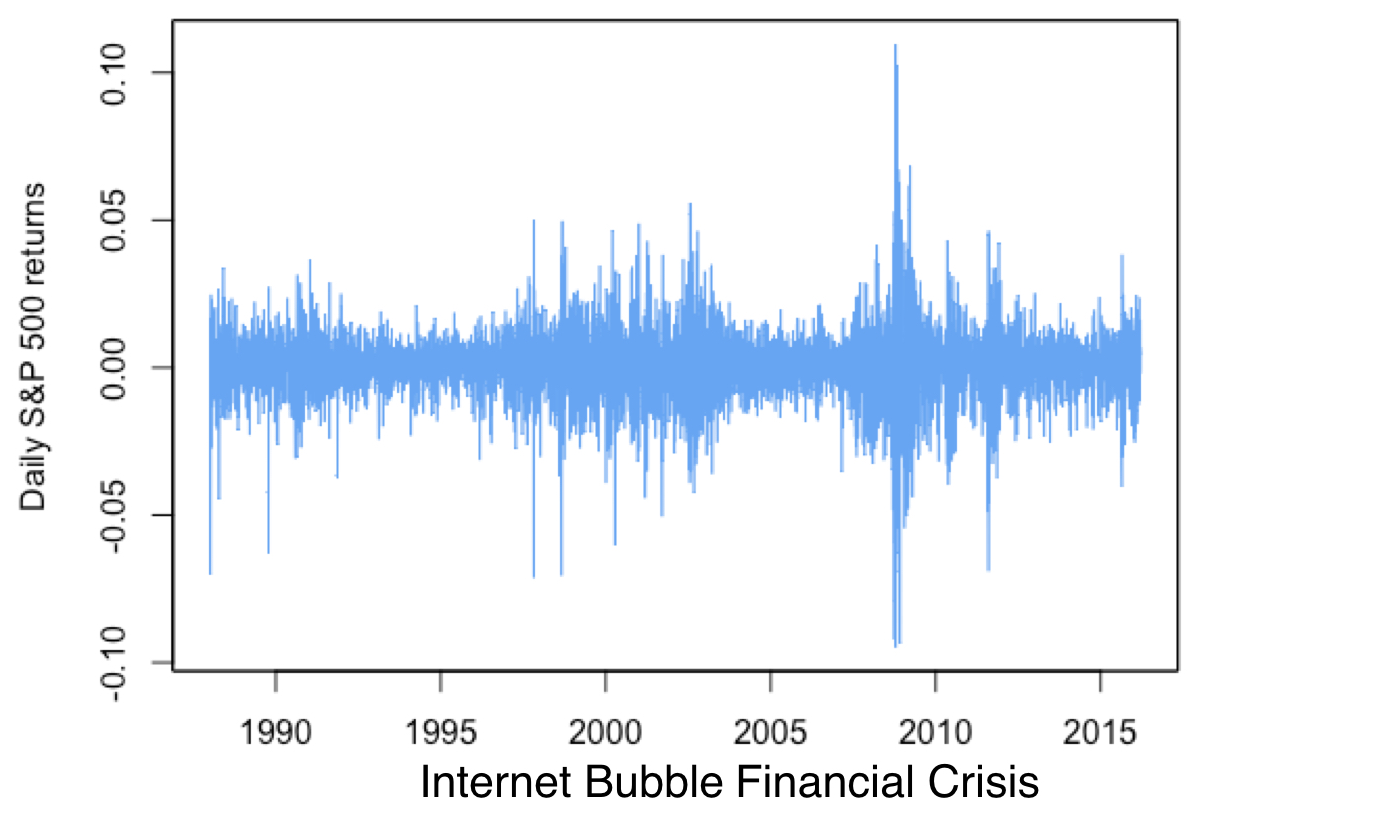

Clusters of high & low volatility

Performance statistics in action

Performance statistics in action

Performance statistics in action

Performance statistics in action

Performance statistics in action

Performance statistics in action

Performance statistics in action

Performance statistics in action

Rolling estimation samples

- Rolling samples of K observations:

- Discard the most distant and include the most recent

Rolling estimation samples

- Rolling samples of K observations:

- Discard the most distant and include the most recent

Rolling estimation samples

- Rolling samples of K observations:

- Discard the most distant and include the most recent

Rolling estimation samples

- Rolling samples of K observations:

- Discard the most distant and include the most recent

Rolling estimation samples

- Rolling samples of K observations:

- Discard the most distant and include the most recent

Rolling estimation samples

- Rolling samples of K observations:

- Discard the most distant and include the most recent

Rolling estimation samples

- Rolling samples of K observations:

- Discard the most distant and include the most recent

Rolling performance calculation